"The 3rd ground is based on the fact of mentioning in the Audit Report a payment of $562,500.00 by the Government to the plaintiffs. The amount of $562,500 was inclusive of $62,500.00 paid as VAT. The learned counsel for the defendant submitted that in the Final Audit Report this amount had been revised to $500,000.00. The learned counsel for the plaintiffs submitted that the plaintiffs did not get the entire amount as the plaintiffs had to make payments to others as well. However it appears that the payment of $500,000.00 was made to the plaintiffs and therefore the plaintiffs cannot complain."

The Fiji Court of Appeal, November 2019

The Fiji Court of Appeal, November 2019

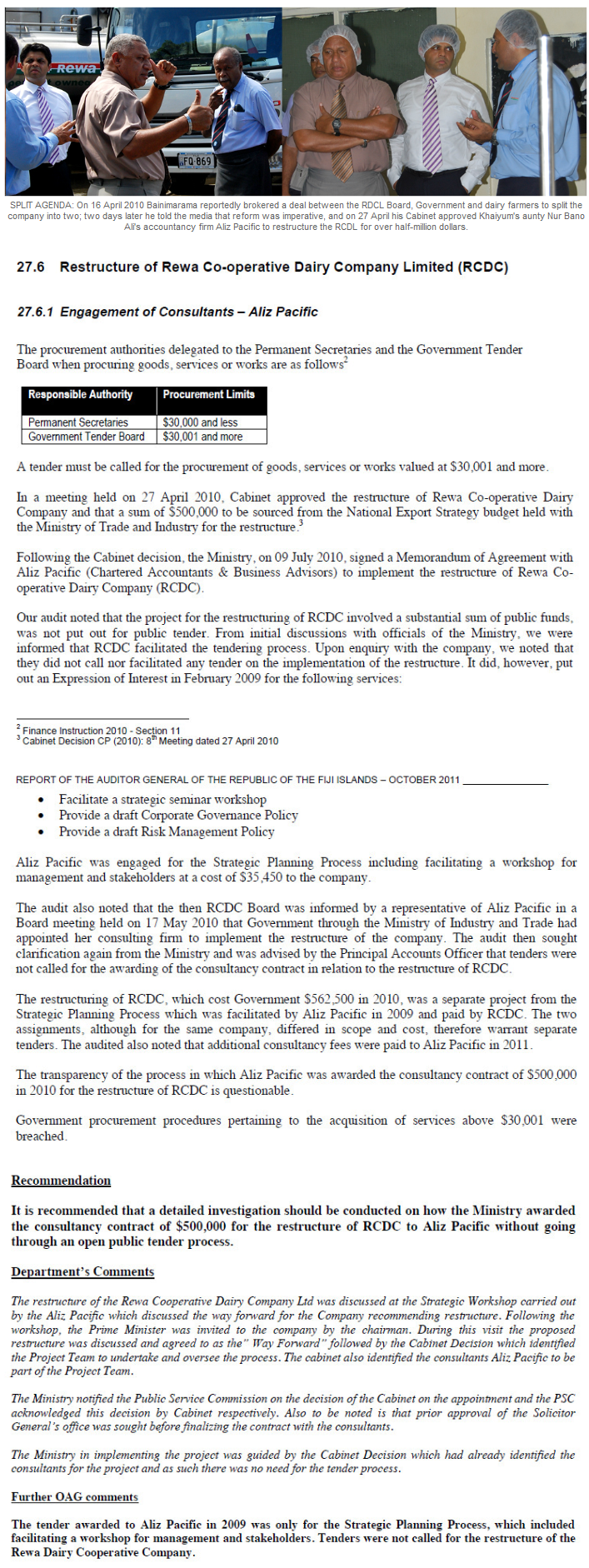

Fijileaks: By running to the Fiji High Court, all debate on the Fiji Auditor-General's 2010 Report on Rewa Dairy and her company's consultany fees without the tender process was KILLED OFF in the Fiji Press and Social Media, only for both, Fiji High Court (2018) and Fiji Court of Appeal (2019), to throw out her claims that the Report's contents were defamatory and malicious to her and to Aliz Pacific

"The plaintiffs [Aliz Pacific and Dr Nur Bao Ali] state that now they are viewed with suspicion and distrust which is causing them and their employees mental injury, stress and harm. The plaintiffs state that the second plaintiff also holds various other positions within society and the media outcry arising from the Defendant’s [Fiji Auditor General] Audit report has caused her deep embarrassment, damage to her reputation and stress."

Fijileaks: The $500,000 was taken out of the Export Growth Facility Fund. Rewa Dairy survives because it imports powder and reconstitutes it in Fiji for selling. That is what made it profitable because of duty concessions to Rew Dairy, which became owned by CJPatel. Hence, a basic commodity like milk is more expensive for Fiji's consumers

WEARING WITH PRIDE |  |

"Considering the above, I agree with the First Defendant’s [Fiji's Auditor-General] assertion that the said statements were statements of facts and were true in substance and in fact. The comments in the statement were based on the said statement of facts and can be considered as fair comments on a matter of public interest. The First Defendant also submits that the said statements and comments were not published maliciously or with any malicious intent. Having considered all the evidence as a whole, I am of the opinion that the Plaintiffs have failed to establish on a balance of probabilities that the statements and words referred to in paragraph 1.13 of the Agreed Facts (and the additional portion referred to in paragraph 17 of my Judgment) are defamatory of the Plaintiffs and that the statements were published maliciously by the First Defendant. Since, Court has made a determination, that the impugned statements and words are not defamatory of the Plaintiffs, I find it inexpedient to delve into issues 2.4; 2.5; 2.6; 2.9 and 2.10 of the issues for determination by Court as recorded in the Minutes of the Pre-Trial Conference. For the above reasons, I dismiss the First and Second Plaintiff’s claims made against the First Defendant."

FINAL ORDERS

1. This action is dismissed.

2. Considering all the facts and circumstances of this case, I make no order for costs.

Justice Riyaz Hamza, Fiji High Court, 31 January 218, upheld by Fiji Court of Appeal

FINAL ORDERS

1. This action is dismissed.

2. Considering all the facts and circumstances of this case, I make no order for costs.

Justice Riyaz Hamza, Fiji High Court, 31 January 218, upheld by Fiji Court of Appeal

FIJI COURT OF APPEAL DISMISSES HER CLAIMS:

"The plaintiffs state that several articles too were published (in tabloids) based on these audit reports. The Audit Reports and articles are beyond fair comment and are malicious and have been designed specifically to impugn the character and reputation of the plaintiffs. The plaintiffs state that the Report and the articles have brought the plaintiffs into hatred, ridicule and contempt and they have suffered damages as a result. The plaintiffs state that the plaintiffs have also lost clients who were interested in using their services but have decided not to invest as a result of the image painted by the 2010 Audit Report. The plaintiffs state that now they are viewed with suspicion and distrust which is causing them and their employees mental injury, stress and harm. The plaintiffs state that the second plaintiff also holds various other positions within society and the media outcry arising from the Defendant’s Audit report has caused her deep embarrassment, damage to her reputation and stress."

"The plaintiffs state that several articles too were published (in tabloids) based on these audit reports. The Audit Reports and articles are beyond fair comment and are malicious and have been designed specifically to impugn the character and reputation of the plaintiffs. The plaintiffs state that the Report and the articles have brought the plaintiffs into hatred, ridicule and contempt and they have suffered damages as a result. The plaintiffs state that the plaintiffs have also lost clients who were interested in using their services but have decided not to invest as a result of the image painted by the 2010 Audit Report. The plaintiffs state that now they are viewed with suspicion and distrust which is causing them and their employees mental injury, stress and harm. The plaintiffs state that the second plaintiff also holds various other positions within society and the media outcry arising from the Defendant’s Audit report has caused her deep embarrassment, damage to her reputation and stress."

Fijileaks: We are not aware if the Medal Awarding Committee had before it the two Court judgments, for SHE was awarded the Fiji50 Independence Commemorative Medal by the President of Fiji, Jioji Konrote

BOTH the Fiji High Court [31 January 2018] and Fiji Court of Appeal] l [29 November 2019] had dismissed her claim against the Auditor-General that his 2010 Annual Report exposing her accounting company Aliz Pacific and the restructuring of Rewa Dairy were defamatory and libellous to her and her company. The plaintiffs (Nur Bano Ali and Aliz Pacific) averred that the contents of the articles, based on the Report, in the press and social media, in their natural and ordinary meaning were defamatory. In their natural and ordinary meaning the words were understood to mean:

* That the plaintiffs had acted with dishonesty and deceit in acting as the Lead Consultants in the Restructure of RCDC. * That their appointment as Lead Consultants was improperly done. * They lacked personal integrity. * That they were paid consultancy fees that was improperly procured by the Government of Fiji. * They had engaged in improper practices in being awarded a tender for consultancy services without complying with Government Tender Procedures. *The plaintiffs had exerted undue influence to obtain a Consultancy Contract to Restructure RCDC.

"The Hearing in this case commenced with the Second Plaintiff, Dr. Nur Bano Ali giving evidence on behalf of the Plaintiffs. In her evidence, she re-stated what was submitted by her in the Statement of Claim and all what was recorded by way of the agreed facts in the Minutes of the Pre-Trial Conference.The Plaintiffs also called Mr. Sunil Deo Sharma as a witness. Mr Sharma is a Chartered Accountant and Partner in the First Plaintiff’s Firm." Fiji High Court, 31 January 2018

Aliz Pacific v Auditor General [2019] FJCA 244; ABU004.2018 (29 November 2019)

IN THE COURT OF APPEAL, FIJI

ON APPEAL FROM THE HIGH COURT OF FIJI

CIVIL APPEAL NO. ABU 0004 of 2018

(High Court of Suva Civil Action No. HBC 337 of 2014)

BETWEEN:

ALIZ PACIFIC

1ST Appellant (1ST Plaintiff)

AND:

DR. NUR BANO ALI

2ND Appellant (2ND Plaintiff)

AND:

THE AUDITOR GENERAL OF FIJI

1ST Respondent (1st Defendant)

AND :

THE ATTORNEY GENERAL OF FIJI

2ND Respondent (2nd Defendant)

Coram : Basnayake JA

Lecamwasam JA

Dayaratne JA

Counsel: Mr. D. Sharma for the Appellants

Mr. P. Knight for the 1st Respondent

Ms. O. Solimailagi for the 2nd Respondent

Date of Hearing : 19 November 2019

Date of Judgment: 29 November 2019

JUDGMENT

Basnayake JA

[1] The appellants (1st and 2nd plaintiffs and hereinafter referred to as the plaintiffs) are seeking to have the judgment (pgs. 6-25 of the Record of the High Court (RHC)) dated 31 January 2018 of the learned High Court Judge set aside and to enter judgment as prayed for in the writ of summons (pgs. 26 to 38 RHC). The plaintiffs have tendered six grounds of appeal.

The plaintiff’s case

[2] In the statement of claim (pgs. 28-38 RHC) the plaintiffs have inter alia sought an injunction, a declaration that the 1st defendant (1st respondent) hereinafter referred to as the defendant)) has defamed the plaintiffs, an order that the defendant make a public apology, general and special damages, interest and costs. The plaintiffs state that the defendant in volume 2 of the 2010 Audit Report under the heading, Ministry of Industry and Trade states that, “Tenders were not called for the restructure of the Rewa Co-operative Dairy Company Limited (RCDC) casting doubt on the transparency of the process in awarding the consultancy contract to Aliz Pacific (Plaintiffs). In 2010, the Government paid $562,500.00 to Aliz Pacific in consultancy fees, with additional fees paid in 2011”.

[3] In volume 4 of the 2010 Audit Report the defendant further states, that “Government procurement procedure pertaining to the acquisition of services above $30,001 were breached and the transparency of the process in which Aliz Pacific was awarded the consultancy contract for the restructure of RCDC was questionable. A tender must be called for the procurement of goods services or works valued at $30,001 and more”. “The audit also noted that the then RCDC Board (Rewa Co-operative Dairy Company Limited) was informed by a representative of AP Consultants in a board meeting on 17th May 2010 that the Government through the Ministry of Industry and Trade had appointed her consultancy firm to implement the restructure of the company”.

[4] The plaintiffs aver that the statements and words in the 2010 Audit Report are in fact defamatory and libelous of the plaintiffs. The plaintiffs aver that the contents of the articles in their natural and ordinary meaning are defamatory. In their natural and ordinary meaning the words were understood to mean:

[6] The plaintiff complained that the Audit Report for the year 2010 was tabled in Parliament on 17 October 2014 and circulated through the Defendant’s official website. The members of the public could access the website and make printouts. Thus the 2010 Audit Report was widely circulated through several News Papers.

The Defence

[7] The defendant in his defence (pgs. 41-44 RHC) admitted the relevant statements, the fact that the statements were made in reference to the plaintiff and to its publication. The defendant denied that the statements were defamatory or libelous. The defendant stated that the contents of those statements are true in substance and in fact and insofar as they consist of expressions of opinion, they are fair comments made without malice on the said facts, which are a matter of public interest.

[8] The defendant states that tenders were not called for the restructure of RCDC although the Finance Instructions 2010 provide that tenders must be called for the procurement of goods, services or works valued at $30,001.00 and more. The Government did pay the plaintiff $562,500.00 in 2010 in consultancy fees. The defendant claimed that the publication of the 2010 Report was covered by qualified privilege.

[9] The plaintiff in reply (pgs. 46-47) stated that the defamation arose from the fact of publishing the Report in the defendant’s websites.

Judgment

[10] The learned Judge set out the following two questions for determination;

[11] The learned Judge states that the defendant claims that, the said statements were statements of facts and were factually correct and the comments in the statements were fair comments on a matter of public interest. The learned Judge having considered the Exhibit marked D3, a letter from RCDC to the defendant dated 9 March 2011 concluded on the following two matters, namely; (1). Tenders were not called for the restructure of the Rewa Dairy Corporative Company Limited. (2). That the RCDC Board was informed by a representative of AP Consultants in a Board Meeting held on 17 May 2010 that the Government through the Ministry of Industry and Trade had appointed the First Plaintiff’s consultancy Firm to implement the restructure of the company.

[12] As per the Minutes of the Pre-Trial Conference paragraph 1.9 states that the Government of Fiji paid the 1st Plaintiff $562,500.00 including VAT of $62,500.00 for the services rendered pursuant to the Memorandum of Agreement. Based on this admission the learned Judge found that the statement that the Government did pay Aliz Pacific $562,500.00 in 2010 in consultancy fees is factually correct.

[13] The learned Judge thereafter considered the issue of not calling for tenders. In paragraph 26 of the judgment the learned Judge states that, “The fact that a tender must be called for the procurement of goods, services or works valued at $30,001.00 and more is based on the Finance Instructions 2010”.

[14] The learned Judge concludes in paragraph 30 of his judgment that the impugned statements and words are not defamatory of the plaintiffs and the statements were not published maliciously by the defendant. The learned Judge states that, “In view of the above findings, I find it inexpedient to delve into issues 2.4; 2.5; 2.6; 2.9; and 2.10 for determination”. Those issues are as follows, namely;

2.4: Did the statements, in their natural and ordinary meaning, mean or were understood to mean;

(i). That the plaintiffs had acted with dishonesty and deceit in acting as the Lead Consultants in the Restructure of RCDC.

(ii). That their appointment as Lead Consultants was improperly done.

(iii). That they lacked personal integrity.

(iv). That they were paid consultancy fees that was improperly procured by the Government of Fiji.

(v). That they had engaged in improper practices in being awarded a tender for consultancy services without complying with Government Tender Procedures.

(vi). That the plaintiffs had exerted undue influence to obtain a Consultancy Contract to Restructure RCDC.

2.5 Have the statements brought the plaintiffs into hatred, ridicule and contempt and have they suffered damages as a result?

2.6 Have the plaintiffs lost clients as a result of the publication of the statements?

2.9 Was the publication of the 2010 Audit Report an occasion of qualified privilege?

2.10 What damages, if any, is the First Defendant liable to pay the plaintiffs?

The Grounds of Appeal

[15] i. That the Learned Judge has erred in fact and in law when at paragraph 26 and 27 of the Judgment he held that for this case a tender had to be called for the procurement of goods, services or works valued at $30,001 pursuant to section 11 of the Finance Instructions 2010 without considering the fact that the Finance Instructions 2010 were not in force at the material time and that the Government of Fiji was not a budget sector agency to whom the Finance Instructions 2010 applied.

[16] The learned counsel for the plaintiffs submitted that there is no requirement to call for tenders. Tenders were required as per Financial Instructions 2010 section 11 according to which tenders must be called for the procurement of goods, services or works valued at $30,001.00 and more. The learned counsel submitted that the 2010 Financial Instructions came into force on 1 December 2010 and are therefore not applicable to this case. The learned counsel submitted that the Ministry of Trade and Industry which administered the fund expressed the view that a tender was not required in this case.

[17] The learned counsel submitted that in terms of section 31 of the Management Act 2004 the Finance Instructions apply to and are to be complied with by budget sector agencies. According to section 2 of the Act budget sector agency means a State entity. The learned counsel submitted that the Government is not a budget sector agency and therefore the Financial Instructions have no application. A tender becomes necessary only if a consultant had not been already selected.

[18] The learned counsel also submitted that the Government did not pay $562,500.00 to the plaintiffs. The plaintiff had to make payments to other consultants employed by her. The learned counsel complained about the publication of the report in the official website of the defendant. He submitted that section 152 of the Constitution does not allow the public to have access to the reports of the defendant. The learned counsel also submitted that the comments of the defendant contravened section 152 (2) (a) & (b) of the 2013 Constitution. The learned counsel also submitted that the learned Judge erred in not considering the fact that it was not the defendant who informed at the meeting on 17 July 2010 that the plaintiffs were appointed as consultants.

Submissions of the learned counsel for the defendant

[19] Referring to the tender procedure the learned counsel submitted that it was Finance Instructions 2005 that was in operation during the relevant period according to which tenders need to be called for services costing more than $50,001.00 that are procured by the Government. However no tenders were called for the contract dated 11 July 2010 by which Aliz Pacific was engaged by the Government to act as consultants in the restructure of RCDC. The learned counsel admitted the receipt of letter dated 24 June 2011 from the Ministry of Industry and Trade with the information that there was no need for a tender process as the Cabinet has already identified the consultant for the restructure project. However the defendant as the Auditor General having found that the engagement involved Government expenditure was reasonable to conclude that tenders should have been called for. It was further submitted that the Cabinet Memorandum contained in the agreed bundle of documents No. 6 required the need to call for tenders in the event of needing external services.

[20] With regard to ground No. 6, the learned counsel submitted that by the letter dated 9 March 2011 (pg. 160 of the RHC) the Chief Executive Officer/Company Secretary of RCDC informed the defendant that at the Board Meeting held on 17 May 2010 the 2nd plaintiff advised the members that the Government of Fiji through the Ministry of Industry and Trade had appointed her Consulting firm to be the consultant for the restructure of RCDC. The learned counsel submitted that the evidence of Mr. Hirdhay Lakhan at pg. 592 of the Record (HCR) confirmed the presence of the 2nd plaintiff at the Board Meeting. The learned counsel submitted that there was no room for the defendant to be suspicious of the response of the secretary to the Board of the RCDC on this matter.

[21] Referring to the amount of $562,500.00 the learned counsel submitted that this amount was mentioned in the draft audit report. The amount paid to the plaintiffs as consulting fees were revised to $500,000.00 in the Final Audit Report that was submitted to the Parliament. The amount, $62,500.00 was removed from the Final Report on finding that this was in respect of VAT. The learned counsel submitted that section 167 of the 1997 Constitution, section 152 of the 2013 Constitution and the Audit Act spelt out the duties and responsibilities of the Auditor General. In terms of those provisions the Auditor General is required to audit all expenditure by the Government or State of Fiji. The Auditor General is also required to send copies of these reports to the Minister of Finance for tabling in Parliament.

[22] The learned counsel submitted that the statements referred to by the plaintiffs in the statement of claim are true in that

a). tenders were not called for the restructure of RCDC;

b). the Government did pay Aliz Pacific $562,500.00 in 2010 in consultancy fees;

[24] The learned counsel submitted that the words complained of were more a criticism of the Government in not calling tenders than a criticism of the plaintiffs. The learned counsel submitted that the statements in question are true, made in the discharge of duties cast upon the defendant by law, made without any kind of malice. The learned counsel further submitted that apart from the truth, the comments made are fair and in the interest of public. The learned counsel moves to dismiss the appeal with costs.

Analysis

First Ground of Appeal

[25] The learned counsel for the plaintiffs has taken the best part of his submissions to address court on ground No. 1. The other grounds were not given the same prominence. This shows the significance of ground No. 1. This ground relates to Financial Instructions and budget sector agencies. According to the defendant this audit was in fact done as per the Financial Instructions of 2010. These financial instructions came into force only on 1 December 2010. The contract between the plaintiffs and the Government of Fiji had been entered into on 11 July 2010. Therefore the Financial Instructions of 2010 will have no force. The submission of the learned counsel is that since the Audit Report is based on the Financial Instructions of 2010 and if those Financial Instructions are not relevant the entire Audit Report concerning the plaintiffs should be rejected. In that event the Audit report was made by the defendant without any basis and maliciously.

[26] The learned counsel’s submission is that the defendant cannot now rely on the Financial Instructions of 2005. This was never an issue at the trial. There was no pleading based on this issue. No issue has been raised at the pre-trial conference either on this matter. However the learned counsel concedes that it was the Financial Instructions of 2005 that was in force. The difference between the two Financial Instructions is that, whilst the 2005 Instructions require tenders to be called on Government procurements for services over and above $50,001.00, in the 2010 Financial Instructions the procurement limit has been lowered to $30,001. The amount involved in this case is ten times over the 50,000 limit. Therefore under whatever Instructions the Audit report was made, this contract cannot escape the requirement of having to go through the tender procedure.

[27] I am not able to accept the argument that the Audit report should be rejected. Although the report is based on the 2010 instructions, if the 2010 instructions were not in force, it is plausible to apply the law that was in force at that time. The law in force was the 2005 Financial Instructions where the limit was $50,001.00 and above. The amount involved in this case is $500,000.00.

[28] The learned counsel for the plaintiffs submitted that under the Financial Management Act the Financial Instructions could apply only to budget sector agencies. As the Government is not a budget sector agency, the Financial Instructions have no application and ultimately that the defendant has done something not permitted by law. This is a new matter that the learned counsel is raising for the first time and cannot be permitted. In any event the issue to be determined in this case is not about the Financial Instructions or its applicability to state entities. That becomes relevant only in determining as to whether the conduct of the defendant was actuated by malice or whether it was a fair comment. Therefore the first ground fails.

Second Ground of Appeal

[29] The learned counsel submitted that as the defendant published his report in spite of the instructions given by the Ministry of Industry and Trade that tenders need not apply to this contract, the defendant acted maliciously. The learned counsel for the defendant in his submissions made it clear to court the functions and duties of the defendant. The defendant having admitted the receipt of the instructions from the Trade Ministry has scrutinized this contract in the discharge of his public duty.

[30] It must be appreciated that the defendant did not make his observations in a vacuum. He had set out the background and the basis upon which he was making his observations. The defendant acted in pursuance of the statutory duties entrusted to him. The observations so made, under the circumstances cannot be classified as malicious conduct. Malice cannot be imputed on the failure to adhere to some instructions. This ground has to be rejected as it is without merit.

Third Ground of Appeal

[31] The 3rd ground is based on the fact of mentioning in the Audit Report a payment of $562,500.00 by the Government to the plaintiffs. The amount of $562,500 was inclusive of $62,500.00 paid as VAT. The learned counsel for the defendant submitted that in the Final Audit Report this amount had been revised to $500,000.00. The learned counsel for the plaintiffs submitted that the plaintiffs did not get the entire amount as the plaintiffs had to make payments to others as well. However it appears that the payment of $500,000.00 was made to the plaintiffs and therefore the plaintiffs cannot complain.

Fourth Ground of Appeal

[32] The learned counsel complained of the defendant publishing the report in his website apart from forwarding it to Parliament. The defendant’s position on this is that it was a practice to publish all the reports in his website. However after the complaint the defendant had withdrawn from his website the report relating to the plaintiffs. The learned counsel for the defendant however submitted that the report was published in the Parliament website and the public has access to it. Considering the defenses the defendant took, namely, the truth, fair comment and the public importance, I am of the view that this ground is without merit.

Fifth Ground of Appeal

[33] With regard to this ground I have already answered. Considering the public duty performed by the defendant the defendant was duty bound to comment on certain transactions which the defendant found inappropriate and damaging. This ground is without merit.

Sixth Ground of Appeal

[34] A detail account had been given on this ground by the learned counsel for the defendant. In this case on a query made by the defendant from RCDC over something that occurred at a Board Meeting the defendant had received a reply from none other than the Board Secretary who was also the Chief Executive Officer. The Secretary would have replied to the defendant after perusal of the Board Minutes. Although there is no evidence on this, I am of the view that the decision of the defendant was based on this reply to the effect that it was the 2nd plaintiff who informed the Board that she was appointed by the Government as a consultant in the restructure of RCDC. The learned counsel for the plaintiffs submitted that a witness testified in court that the pronouncement was made by the Chairman, RCDC. However, the witness gave evidence from his recollection. I am of the view that the defendant cannot be held responsible for believing the writing of the Board Secretary on something that occurred during a Board Meeting. Therefore this ground too has to be rejected.

[35] Having considered it in favour of the defendant with regard to the truth of the statements, fair comments on a matter of public importance and in the discharge of his high official duty, I am of the view that the learned Judge rightly dismissed the plaintiffs’ action. Having considered all the grounds against the appellant, this appeal is dismissed with costs in a sum of $5000.00.

Lecamwasam JA

[36] I agree with the reasons and conclusions arrived at by Basnayake JA.

Dayaratne JA

[37] I have read in draft, the judgment of Basnayake JA and agree with his reasons and conclusions.

The Order of the Court are:

Hon. Justice E. Basnayake

JUSTICE OF APPEAL

..................................................

Hon. Justice S. Lecamwasam

JUSTICE OF APPEAL

.....................................

Hon. Justice V. Dayaratne

JUSTICE OF APPEAL

IN THE COURT OF APPEAL, FIJI

ON APPEAL FROM THE HIGH COURT OF FIJI

CIVIL APPEAL NO. ABU 0004 of 2018

(High Court of Suva Civil Action No. HBC 337 of 2014)

BETWEEN:

ALIZ PACIFIC

1ST Appellant (1ST Plaintiff)

AND:

DR. NUR BANO ALI

2ND Appellant (2ND Plaintiff)

AND:

THE AUDITOR GENERAL OF FIJI

1ST Respondent (1st Defendant)

AND :

THE ATTORNEY GENERAL OF FIJI

2ND Respondent (2nd Defendant)

Coram : Basnayake JA

Lecamwasam JA

Dayaratne JA

Counsel: Mr. D. Sharma for the Appellants

Mr. P. Knight for the 1st Respondent

Ms. O. Solimailagi for the 2nd Respondent

Date of Hearing : 19 November 2019

Date of Judgment: 29 November 2019

JUDGMENT

Basnayake JA

[1] The appellants (1st and 2nd plaintiffs and hereinafter referred to as the plaintiffs) are seeking to have the judgment (pgs. 6-25 of the Record of the High Court (RHC)) dated 31 January 2018 of the learned High Court Judge set aside and to enter judgment as prayed for in the writ of summons (pgs. 26 to 38 RHC). The plaintiffs have tendered six grounds of appeal.

The plaintiff’s case

[2] In the statement of claim (pgs. 28-38 RHC) the plaintiffs have inter alia sought an injunction, a declaration that the 1st defendant (1st respondent) hereinafter referred to as the defendant)) has defamed the plaintiffs, an order that the defendant make a public apology, general and special damages, interest and costs. The plaintiffs state that the defendant in volume 2 of the 2010 Audit Report under the heading, Ministry of Industry and Trade states that, “Tenders were not called for the restructure of the Rewa Co-operative Dairy Company Limited (RCDC) casting doubt on the transparency of the process in awarding the consultancy contract to Aliz Pacific (Plaintiffs). In 2010, the Government paid $562,500.00 to Aliz Pacific in consultancy fees, with additional fees paid in 2011”.

[3] In volume 4 of the 2010 Audit Report the defendant further states, that “Government procurement procedure pertaining to the acquisition of services above $30,001 were breached and the transparency of the process in which Aliz Pacific was awarded the consultancy contract for the restructure of RCDC was questionable. A tender must be called for the procurement of goods services or works valued at $30,001 and more”. “The audit also noted that the then RCDC Board (Rewa Co-operative Dairy Company Limited) was informed by a representative of AP Consultants in a board meeting on 17th May 2010 that the Government through the Ministry of Industry and Trade had appointed her consultancy firm to implement the restructure of the company”.

[4] The plaintiffs aver that the statements and words in the 2010 Audit Report are in fact defamatory and libelous of the plaintiffs. The plaintiffs aver that the contents of the articles in their natural and ordinary meaning are defamatory. In their natural and ordinary meaning the words were understood to mean:

- That the plaintiffs had acted with dishonesty and deceit in acting as the Lead Consultants in the Restructure of RCDC.

- That their appointment as Lead Consultants was improperly done.

- They lacked personal integrity.

- That they were paid consultancy fees that was improperly procured by the Government of Fiji.

- They had engaged in improper practices in being awarded a tender for consultancy services without complying with Government Tender Procedures.

- The plaintiffs had exerted undue influence to obtain a Consultancy Contract to Restructure RCDC.

[6] The plaintiff complained that the Audit Report for the year 2010 was tabled in Parliament on 17 October 2014 and circulated through the Defendant’s official website. The members of the public could access the website and make printouts. Thus the 2010 Audit Report was widely circulated through several News Papers.

The Defence

[7] The defendant in his defence (pgs. 41-44 RHC) admitted the relevant statements, the fact that the statements were made in reference to the plaintiff and to its publication. The defendant denied that the statements were defamatory or libelous. The defendant stated that the contents of those statements are true in substance and in fact and insofar as they consist of expressions of opinion, they are fair comments made without malice on the said facts, which are a matter of public interest.

[8] The defendant states that tenders were not called for the restructure of RCDC although the Finance Instructions 2010 provide that tenders must be called for the procurement of goods, services or works valued at $30,001.00 and more. The Government did pay the plaintiff $562,500.00 in 2010 in consultancy fees. The defendant claimed that the publication of the 2010 Report was covered by qualified privilege.

[9] The plaintiff in reply (pgs. 46-47) stated that the defamation arose from the fact of publishing the Report in the defendant’s websites.

Judgment

[10] The learned Judge set out the following two questions for determination;

- Are the statements and words set out in paragraph 1.13 of the Agreed Facts defamatory of the plaintiffs?

[11] The learned Judge states that the defendant claims that, the said statements were statements of facts and were factually correct and the comments in the statements were fair comments on a matter of public interest. The learned Judge having considered the Exhibit marked D3, a letter from RCDC to the defendant dated 9 March 2011 concluded on the following two matters, namely; (1). Tenders were not called for the restructure of the Rewa Dairy Corporative Company Limited. (2). That the RCDC Board was informed by a representative of AP Consultants in a Board Meeting held on 17 May 2010 that the Government through the Ministry of Industry and Trade had appointed the First Plaintiff’s consultancy Firm to implement the restructure of the company.

[12] As per the Minutes of the Pre-Trial Conference paragraph 1.9 states that the Government of Fiji paid the 1st Plaintiff $562,500.00 including VAT of $62,500.00 for the services rendered pursuant to the Memorandum of Agreement. Based on this admission the learned Judge found that the statement that the Government did pay Aliz Pacific $562,500.00 in 2010 in consultancy fees is factually correct.

[13] The learned Judge thereafter considered the issue of not calling for tenders. In paragraph 26 of the judgment the learned Judge states that, “The fact that a tender must be called for the procurement of goods, services or works valued at $30,001.00 and more is based on the Finance Instructions 2010”.

[14] The learned Judge concludes in paragraph 30 of his judgment that the impugned statements and words are not defamatory of the plaintiffs and the statements were not published maliciously by the defendant. The learned Judge states that, “In view of the above findings, I find it inexpedient to delve into issues 2.4; 2.5; 2.6; 2.9; and 2.10 for determination”. Those issues are as follows, namely;

2.4: Did the statements, in their natural and ordinary meaning, mean or were understood to mean;

(i). That the plaintiffs had acted with dishonesty and deceit in acting as the Lead Consultants in the Restructure of RCDC.

(ii). That their appointment as Lead Consultants was improperly done.

(iii). That they lacked personal integrity.

(iv). That they were paid consultancy fees that was improperly procured by the Government of Fiji.

(v). That they had engaged in improper practices in being awarded a tender for consultancy services without complying with Government Tender Procedures.

(vi). That the plaintiffs had exerted undue influence to obtain a Consultancy Contract to Restructure RCDC.

2.5 Have the statements brought the plaintiffs into hatred, ridicule and contempt and have they suffered damages as a result?

2.6 Have the plaintiffs lost clients as a result of the publication of the statements?

2.9 Was the publication of the 2010 Audit Report an occasion of qualified privilege?

2.10 What damages, if any, is the First Defendant liable to pay the plaintiffs?

The Grounds of Appeal

[15] i. That the Learned Judge has erred in fact and in law when at paragraph 26 and 27 of the Judgment he held that for this case a tender had to be called for the procurement of goods, services or works valued at $30,001 pursuant to section 11 of the Finance Instructions 2010 without considering the fact that the Finance Instructions 2010 were not in force at the material time and that the Government of Fiji was not a budget sector agency to whom the Finance Instructions 2010 applied.

- That the Learned Judge has erred in fact and in law when at paragraph 28 of the Judgment he held that the statements made by the First Respondent were not published maliciously or with any malicious intent without considering the fact that the First Respondent ignored the advice of the Ministry of Trade and Industry who had informed the First Respondent that a tender was not necessary in the case and also without taking any steps to verify the allegations made in his report with the Plaintiffs so as to give them an opportunity to refute the allegations before the same was published in his Report by the First Respondent.

- That the Learned Judge has erred in fact and in law in failing to uphold the Appellant’s submission that the Government of Fiji paid the sum of $562,500.00 to Aliz Pacific to facilitate the Consultancy and that the First Respondent wanted to give the readers of his Report the distinct impression that this amount was paid to Aliz Pacific as their fees when in fact he knew or clearly would have known that this was not so and a portion of the fees were also paid to other entities. Any reasonable reader reading the First Respondent’s Report would think that Aliz Pacific got paid $562,500.00 as their fees. In doing so the First Respondent has withheld information in his Report that the fees were apportioned among other professionals. The clear inference here is that that was so because it was his intention to malign the Appellants.

- That the Learned Judge has erred in fact and in law in failing to consider and uphold the Appellant’s submissions that the Constitution only protected the Auditor General if he complied with the Constitution and submitted his Report in Parliament only to the Speaker and the Ministry of Finance and that nothing in s.152(13) of the Constitution allowed the Auditor General to place the Audit Report in his Website where members of the public can have access to the same.

- That the Learned Judge has erred in fact and in law in failing to consider and uphold the Appellant’s submissions that the First Respondent was carrying out a statutory duty to compile his Report for the Parliament of Fiji but any comment that the First Respondent made in the Report had to be on the matters that he was required to give an opinion in pursuant to section 152(2)(a) and (b) of the 2013 Constitution and that the First Respondent deliberately failed to comply with s.152(2)(a) and (b) in order to enhance his malicious attack against the Appellants.

- That the Learned Judge has erred in fact and in law in failing to uphold the Appellant’s submissions and consider the evidence before the Court that the Second Appellant did not inform the Board of Directors of Rewa Co-operative Dairy Company Limited Board that her Company had been awarded a Consultancy and that this was done by one Amrita Singh.”

[16] The learned counsel for the plaintiffs submitted that there is no requirement to call for tenders. Tenders were required as per Financial Instructions 2010 section 11 according to which tenders must be called for the procurement of goods, services or works valued at $30,001.00 and more. The learned counsel submitted that the 2010 Financial Instructions came into force on 1 December 2010 and are therefore not applicable to this case. The learned counsel submitted that the Ministry of Trade and Industry which administered the fund expressed the view that a tender was not required in this case.

[17] The learned counsel submitted that in terms of section 31 of the Management Act 2004 the Finance Instructions apply to and are to be complied with by budget sector agencies. According to section 2 of the Act budget sector agency means a State entity. The learned counsel submitted that the Government is not a budget sector agency and therefore the Financial Instructions have no application. A tender becomes necessary only if a consultant had not been already selected.

[18] The learned counsel also submitted that the Government did not pay $562,500.00 to the plaintiffs. The plaintiff had to make payments to other consultants employed by her. The learned counsel complained about the publication of the report in the official website of the defendant. He submitted that section 152 of the Constitution does not allow the public to have access to the reports of the defendant. The learned counsel also submitted that the comments of the defendant contravened section 152 (2) (a) & (b) of the 2013 Constitution. The learned counsel also submitted that the learned Judge erred in not considering the fact that it was not the defendant who informed at the meeting on 17 July 2010 that the plaintiffs were appointed as consultants.

Submissions of the learned counsel for the defendant

[19] Referring to the tender procedure the learned counsel submitted that it was Finance Instructions 2005 that was in operation during the relevant period according to which tenders need to be called for services costing more than $50,001.00 that are procured by the Government. However no tenders were called for the contract dated 11 July 2010 by which Aliz Pacific was engaged by the Government to act as consultants in the restructure of RCDC. The learned counsel admitted the receipt of letter dated 24 June 2011 from the Ministry of Industry and Trade with the information that there was no need for a tender process as the Cabinet has already identified the consultant for the restructure project. However the defendant as the Auditor General having found that the engagement involved Government expenditure was reasonable to conclude that tenders should have been called for. It was further submitted that the Cabinet Memorandum contained in the agreed bundle of documents No. 6 required the need to call for tenders in the event of needing external services.

[20] With regard to ground No. 6, the learned counsel submitted that by the letter dated 9 March 2011 (pg. 160 of the RHC) the Chief Executive Officer/Company Secretary of RCDC informed the defendant that at the Board Meeting held on 17 May 2010 the 2nd plaintiff advised the members that the Government of Fiji through the Ministry of Industry and Trade had appointed her Consulting firm to be the consultant for the restructure of RCDC. The learned counsel submitted that the evidence of Mr. Hirdhay Lakhan at pg. 592 of the Record (HCR) confirmed the presence of the 2nd plaintiff at the Board Meeting. The learned counsel submitted that there was no room for the defendant to be suspicious of the response of the secretary to the Board of the RCDC on this matter.

[21] Referring to the amount of $562,500.00 the learned counsel submitted that this amount was mentioned in the draft audit report. The amount paid to the plaintiffs as consulting fees were revised to $500,000.00 in the Final Audit Report that was submitted to the Parliament. The amount, $62,500.00 was removed from the Final Report on finding that this was in respect of VAT. The learned counsel submitted that section 167 of the 1997 Constitution, section 152 of the 2013 Constitution and the Audit Act spelt out the duties and responsibilities of the Auditor General. In terms of those provisions the Auditor General is required to audit all expenditure by the Government or State of Fiji. The Auditor General is also required to send copies of these reports to the Minister of Finance for tabling in Parliament.

[22] The learned counsel submitted that the statements referred to by the plaintiffs in the statement of claim are true in that

a). tenders were not called for the restructure of RCDC;

b). the Government did pay Aliz Pacific $562,500.00 in 2010 in consultancy fees;

- that under the Finance Instructions, tenders must be called for the procurement of services by the Government valued at $30,001.00 or more (under the 2010 Finance Instructions) or $50,001.00 or more (under the 2005 Finance Instructions);

[24] The learned counsel submitted that the words complained of were more a criticism of the Government in not calling tenders than a criticism of the plaintiffs. The learned counsel submitted that the statements in question are true, made in the discharge of duties cast upon the defendant by law, made without any kind of malice. The learned counsel further submitted that apart from the truth, the comments made are fair and in the interest of public. The learned counsel moves to dismiss the appeal with costs.

Analysis

First Ground of Appeal

[25] The learned counsel for the plaintiffs has taken the best part of his submissions to address court on ground No. 1. The other grounds were not given the same prominence. This shows the significance of ground No. 1. This ground relates to Financial Instructions and budget sector agencies. According to the defendant this audit was in fact done as per the Financial Instructions of 2010. These financial instructions came into force only on 1 December 2010. The contract between the plaintiffs and the Government of Fiji had been entered into on 11 July 2010. Therefore the Financial Instructions of 2010 will have no force. The submission of the learned counsel is that since the Audit Report is based on the Financial Instructions of 2010 and if those Financial Instructions are not relevant the entire Audit Report concerning the plaintiffs should be rejected. In that event the Audit report was made by the defendant without any basis and maliciously.

[26] The learned counsel’s submission is that the defendant cannot now rely on the Financial Instructions of 2005. This was never an issue at the trial. There was no pleading based on this issue. No issue has been raised at the pre-trial conference either on this matter. However the learned counsel concedes that it was the Financial Instructions of 2005 that was in force. The difference between the two Financial Instructions is that, whilst the 2005 Instructions require tenders to be called on Government procurements for services over and above $50,001.00, in the 2010 Financial Instructions the procurement limit has been lowered to $30,001. The amount involved in this case is ten times over the 50,000 limit. Therefore under whatever Instructions the Audit report was made, this contract cannot escape the requirement of having to go through the tender procedure.

[27] I am not able to accept the argument that the Audit report should be rejected. Although the report is based on the 2010 instructions, if the 2010 instructions were not in force, it is plausible to apply the law that was in force at that time. The law in force was the 2005 Financial Instructions where the limit was $50,001.00 and above. The amount involved in this case is $500,000.00.

[28] The learned counsel for the plaintiffs submitted that under the Financial Management Act the Financial Instructions could apply only to budget sector agencies. As the Government is not a budget sector agency, the Financial Instructions have no application and ultimately that the defendant has done something not permitted by law. This is a new matter that the learned counsel is raising for the first time and cannot be permitted. In any event the issue to be determined in this case is not about the Financial Instructions or its applicability to state entities. That becomes relevant only in determining as to whether the conduct of the defendant was actuated by malice or whether it was a fair comment. Therefore the first ground fails.

Second Ground of Appeal

[29] The learned counsel submitted that as the defendant published his report in spite of the instructions given by the Ministry of Industry and Trade that tenders need not apply to this contract, the defendant acted maliciously. The learned counsel for the defendant in his submissions made it clear to court the functions and duties of the defendant. The defendant having admitted the receipt of the instructions from the Trade Ministry has scrutinized this contract in the discharge of his public duty.

[30] It must be appreciated that the defendant did not make his observations in a vacuum. He had set out the background and the basis upon which he was making his observations. The defendant acted in pursuance of the statutory duties entrusted to him. The observations so made, under the circumstances cannot be classified as malicious conduct. Malice cannot be imputed on the failure to adhere to some instructions. This ground has to be rejected as it is without merit.

Third Ground of Appeal

[31] The 3rd ground is based on the fact of mentioning in the Audit Report a payment of $562,500.00 by the Government to the plaintiffs. The amount of $562,500 was inclusive of $62,500.00 paid as VAT. The learned counsel for the defendant submitted that in the Final Audit Report this amount had been revised to $500,000.00. The learned counsel for the plaintiffs submitted that the plaintiffs did not get the entire amount as the plaintiffs had to make payments to others as well. However it appears that the payment of $500,000.00 was made to the plaintiffs and therefore the plaintiffs cannot complain.

Fourth Ground of Appeal

[32] The learned counsel complained of the defendant publishing the report in his website apart from forwarding it to Parliament. The defendant’s position on this is that it was a practice to publish all the reports in his website. However after the complaint the defendant had withdrawn from his website the report relating to the plaintiffs. The learned counsel for the defendant however submitted that the report was published in the Parliament website and the public has access to it. Considering the defenses the defendant took, namely, the truth, fair comment and the public importance, I am of the view that this ground is without merit.

Fifth Ground of Appeal

[33] With regard to this ground I have already answered. Considering the public duty performed by the defendant the defendant was duty bound to comment on certain transactions which the defendant found inappropriate and damaging. This ground is without merit.

Sixth Ground of Appeal

[34] A detail account had been given on this ground by the learned counsel for the defendant. In this case on a query made by the defendant from RCDC over something that occurred at a Board Meeting the defendant had received a reply from none other than the Board Secretary who was also the Chief Executive Officer. The Secretary would have replied to the defendant after perusal of the Board Minutes. Although there is no evidence on this, I am of the view that the decision of the defendant was based on this reply to the effect that it was the 2nd plaintiff who informed the Board that she was appointed by the Government as a consultant in the restructure of RCDC. The learned counsel for the plaintiffs submitted that a witness testified in court that the pronouncement was made by the Chairman, RCDC. However, the witness gave evidence from his recollection. I am of the view that the defendant cannot be held responsible for believing the writing of the Board Secretary on something that occurred during a Board Meeting. Therefore this ground too has to be rejected.

[35] Having considered it in favour of the defendant with regard to the truth of the statements, fair comments on a matter of public importance and in the discharge of his high official duty, I am of the view that the learned Judge rightly dismissed the plaintiffs’ action. Having considered all the grounds against the appellant, this appeal is dismissed with costs in a sum of $5000.00.

Lecamwasam JA

[36] I agree with the reasons and conclusions arrived at by Basnayake JA.

Dayaratne JA

[37] I have read in draft, the judgment of Basnayake JA and agree with his reasons and conclusions.

The Order of the Court are:

- Appeal dismissed.

- The 1st Respondent is entitled to costs $5000.00 to be paid by the Appellants within 28 days.

Hon. Justice E. Basnayake

JUSTICE OF APPEAL

..................................................

Hon. Justice S. Lecamwasam

JUSTICE OF APPEAL

.....................................

Hon. Justice V. Dayaratne

JUSTICE OF APPEAL

From Fijileaks Archive, 3 November 2014