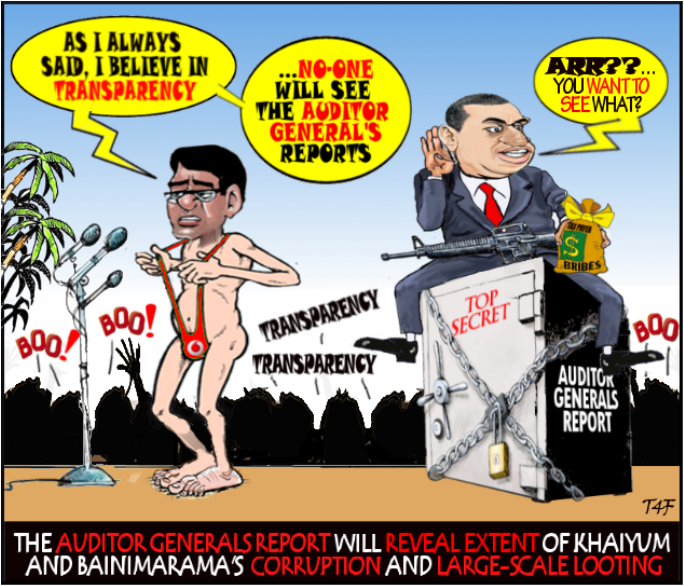

AIYAZ SAYED KHAIYUM: The Auditor-General's Reports will be released a week after the September election results; oh, YES, now we know WHY!

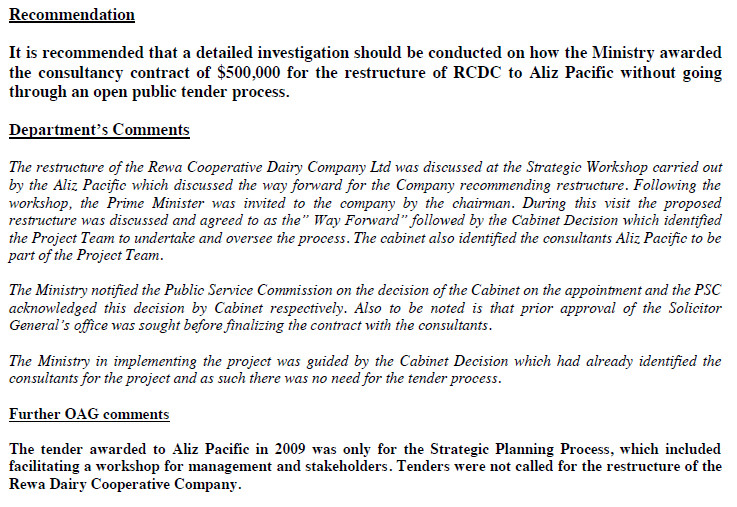

"It is recommended that a detailed investigation should be conducted on how the Ministry awarded the consultancy contract of $500,000 for the restructure of RCDC to Aliz Pacific without going through an open public tender process" - The Auditor-General, 2010

UNDECLARED CONFLICT OF INTEREST: The Ministry of Public Enterprise and Ministry of Industry & Trade came under Aiyaz Khaiyum.

Did Khaiyum declare his interest?

1) Nur Bano Ali - Aunty to Khaiyum and Director of Aliz Pacific;

2) Nur Bano Ali was his accountant (Latifa Holdings);

3) Nur Bano Ali was his (and the Cabinet ministers') paymaster

Bainimarama, Khaiyum and Nur Bano Ali were behaving as if the money in the Government coffers was their own family trust fund to do whatever they liked - but then that is what happens when one gets DICTATORSHIP and the PRESS chooses to become a willing and sedulous concubine!

THE SUN IS YET TO RISE: Rewa Dairy is now under the ownership of Southern Cross Food, Ba, a subsidiary of CJ Patel Group, which also owns the Fiji Sun. No wonder this revelation in the Auditor-General's Report is yet to be reported in the Fiji Sun; instead the regime's news dog hounds in the Fiji Sun are too busy attacking Fijileaks and Victor Lal, the former Fiji Sun opinion columnist and co-winner of the 2008 Robert Keith-Reid Award For Outstanding Journalism. Nur Bano Ali split RCDL into Fiji Dairy Co- Operative Ltd and Government sold Rewa Dairy to CJ Group for $10million. Struggling farmers are still complaining about milk price. Bainimarama supporter Joseva Serulagilagi is the chairman of new struggling farmers co-op company.

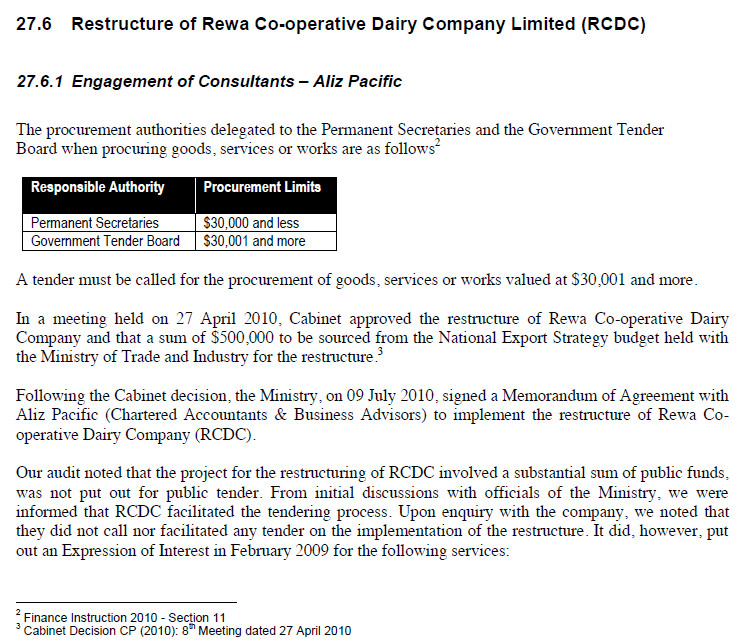

Auditor- General, 2010:

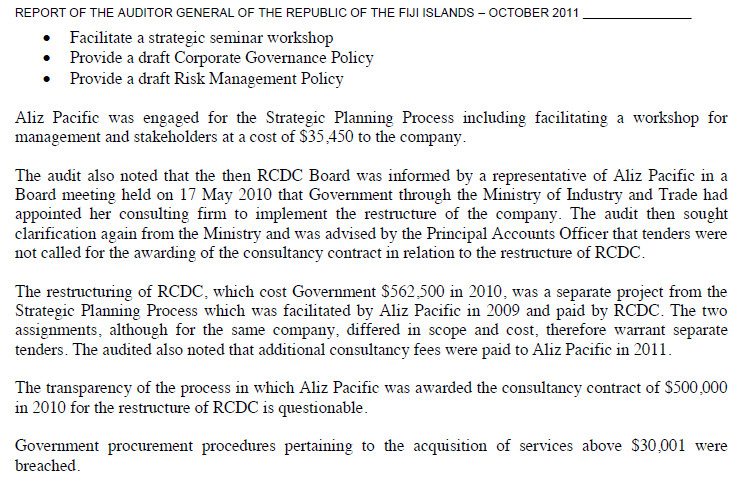

Aliz Pacific was engaged for the Strategic Planning Process including facilitating a workshop for management and stakeholders at a cost of $35,450 to the company. The audit also noted that the then RCDC Board was informed by a representative of Aliz Pacific in a Board meeting held on 17 May 2010 that Government through the Ministry of Industry and Trade had appointed her consulting firm to implement the restructure of the company. The audit then sought clarification again from the Ministry and was advised by the Principal Accounts Officer that tenders were not called for the awarding of the consultancy contract in relation to the restructure of RCDC.

The restructuring of RCDC, which cost Government $562,500 in 2010, was a separate project from the Strategic Planning Process which was facilitated by Aliz Pacific in 2009 and paid by RCDC. The two assignments, although for the same company, differed in scope and cost, therefore warrant separate tenders. The audited also noted that additional consultancy fees were paid to Aliz Pacific in 2011.

The transparency of the process in which Aliz Pacific was awarded the consultancy contract of $500,000 in 2010 for the restructure of RCDC is questionable. Government procurement procedures pertaining to the acquisition of services above $30,001 were breached.

Read A-G's Report on how Aunty's Aliz Pacific 'skimmed-milked' Fiji's taxpayers during Bainimarama/Khaiyum dictatorship!

SPLIT AGENDA: On 16 April 2010 Bainimarama reportedly brokered a deal between the RDCL Board, Government and dairy farmers to split the company into two; two days later he told the media that reform was imperative, and on 27 April his Cabinet approved Khaiyum's aunty Nur Bano Ali's accountancy firm Aliz Pacific to restructure the RCDL for over half-million dollars.

The Auditor-General and the Accountability of Public Expenditure

Address to the Office of the Auditor-General, Fiji

By Nazhat Shameem

5th December 2012

"An institution in trouble will often delay a report of bad news for as long as possible."

Since the parlous state of the bank’s finances became known to the public, there has been a tendency to view the auditor-general as the saviour of the public because it was the qualified audit of the NBF that finally brought the bank’s problems into the open. Yet the fact remained that when the auditor-general ‘blew the whistle’ on the NBF, he blew too softly and too belatedly. It is worth noting that over the 1991 to 1995 period the NBF’s situation was studied frequently by the Reserve Bank. This also raises a crucial issue of cooperation between the Reserve Bank and the auditor-general. What is not in the public record is whether the auditor-general was aware that the NBF was deemed insolvent by the Reserve Bank and whether the Reserve Bank had fully disclosed information about the NBF to the auditor-general.”

Introduction

At the time the National Bank was investigated by the Reserve Bank of Fiji and the Fiji Police Force for possible fraud and corruption, I was the Director of Public Prosecutions. I, the Auditor-General, the Supervisor of Elections, the Commissioner of Police and the Ombudsman were the constitutional officers appointed under the 1990 or 1997 Constitutions and entrusted to hold society to account for abuses of power and public money, or entrusted to protect free elections and human rights. As the NBF investigations gained momentum, so did attempts by the executive to control the constitutional officers. There were attempts to make us accountable to various permanent secretaries in our “performance”, and when we refused, attempts to amend the 1997 Constitution to write in such accountability. Fortunately, the Constitution could not be amended without the support of the Opposition. Such support was refused, and the performance agreements were never signed.

However, the incident reminded me of the importance of the independence of the office of the auditor-general in relation to government bureaucracy. At this time, when Fiji is working towards a new constitutional framework, it is important to remind ourselves that institutional independence in offices designed to hold others accountable, must be strengthened, not weakened, and that the most effective way to undermine the effectiveness of offices such as the Auditor-General’s is to create a bureaucratic form of control over the performance of the auditors. A strong Auditor-General is a most important guard against bad governance. Sadly, Fiji has had a shocking history of bad governance, with risk factors which are specific to Fiji’s business climate and political history.

Our fraud history

We cannot blame the auditors for fraud or corruption. However, the failure to detect fraud and corruption, and the failure to identify the signposts for corruption risks, is a failure of the auditor. How this may manifest itself is sometimes problematic.

In a recent case in the Lautoka High Court Sunbeach Fiji Limited, the company which owns the Trans International Hotel in Nadi brought an action in negligence against its external auditors for failing to detect a fraud of $83,756.11. The action is still pending. The statement of claim alleges that the audits of the two preceding years should have uncovered the fraud. However the auditors said in response that they did highlight weaknesses in the accounting practices of the company in their 2009 and 2010 reports. The reports spoke of internal control procedures which were weak, and of the possibility of potential fraud. The auditors found missing receipt books, missing food and beverage dockets, and a missing front office guest ledger and other weaknesses which indicated a “chronic poor accounting management system at Sunbeach”. However Sunbeach said that simple bank reconciliations would have shown that what should have been in the bank according to the hotel’s accounts, and what was in fact in the bank account for the bank did not correspond. All of this led to an acrimonious exchange of emails between the hotel and Ernst and Young, and finally to the refusal of the auditors to lodge the company’s tax returns, on the grounds that the returns should not have contained accounts signed off by the company when it knew that there had been a fraud on the accounts. The matter went before the Master for discovery of all audit documents in relation to the hotel by the accountants to the hotel. The Master refused the application, calling it a “cleverly disguised fishing expedition” and expressing the view that the plaintiff had no case against the accountants in any event because it had failed to produce evidence that there was indeed a fraud.

Although the case is still pending, it does illustrate the possible disconnection between what auditors think they are supposed to detect, and what their clients think they are supposed to detect. It also illustrates that (in that case the external auditors) auditors are often in the front line for the detection of fraud and corruption, and must learn to recognise the corruption and fraud signposts in order to report accurately to the clients. The first major fraud to be detected in Fiji was the Flour Mills case. That was a case of a company which had special agreements with government to mill enough flour for local consumption in return for exemption from customs duties and ports fees. When the company started to make a significant profit, the Board was afraid that these concessions would be withdrawn by government, and asked the management to falsify the amount of profits and stock the company had, in order to conceal the true state of affairs. This was a criminal offence, and the Financial Controller blew the whistle on the company by writing to the then Prime Minister. The Prime Minister asked an independent auditor to conduct an audit, and the audit commenced with the simplest test of all; an examination of how much wheat was in fact in the silos of the Flour Mills of Fiji. A prosecution followed and led to convictions. However, an appeal against the convictions succeeded, and no retrial was ever conducted.

The National Bank of Fiji was the next major financial scam. Said to have commenced from 1978 to 1985 when the Minister of Finance approved the exemption of the Bank from the rule in the Banking Act that no one customer should be lent more than 25% of a bank’s equity, by 1996 the Bank was owed about $220 million, over 8.5% of GNP. The rot commenced long before the 1987 coup, but events after 1987 lurched from one banking disaster to another. The Bank seemed to be confused about its real role. Was it a development bank, created to implement social justice, or was it a commercial bank? It followed reckless lending policies, ignored internal procedures and sound banking practices and grew rapidly when it lacked the ability to manage such growth. During this reckless history, there was a resounding silence from the internal auditors of the Bank.

So insignificant was the role of internal auditors in the case of the National Bank of Fiji, that it has never got a mention in any of the analyses of the Bank’s collapse. In “Crisis; The Collapse of the National Bank of Fiji” there is much discussion on the role of the Reserve Bank in its failure to stop the bank operating after it was technically insolvent, and on the role of the Auditor-General (who blew the whistle too softly and too late) but not of the role of the internal auditors. Yet the internal auditors must have been instrumental in providing reassuring reports to the Board of Directors that all was well in the State of Denmark. Is it possible that they did not know what was happening? After all, according to Grynberg, Munro and White, “on paper there were more than sufficient safeguards”. In fact, the internal audits could not have missed the widespread disregard for prudent banking procedure, the dishonesty, the loans approved on the telephones and bits of paper, and the inadequate or missing securities. Did they report the irregularities? The lending without adequate securities? The use of patronage to approve loans? We will never know. However from the Auditor- General’s reports, and from the Annual Corporate Reports of the bank, one is able to draw some conclusions about the role of the auditors and accountants in the collapse of the Bank. Michael White said this of audit reports generally; “The accounting profession has come under sustained attack over a long period for its apparent inability to identify imminent corporate collapses through the legally acquired annual corporate reports. A substantial literature points to many examples of organisations reporting profits and a generally solid financial position, applying generally accepted accounting practices, receiving an unqualified audit report, yet proving bankrupt within twelve months of the reporting date.”

We do not know what the internal auditors told their superiors at the Bank but the annual corporate reports failed to mention that the Minister of Finance had given exemption to the Bank from the requirement under the Banking Act that aggregate loans to one customer should not exceed 25% of the bank’s equity. The annual reports showed that the Bank experienced rapid growth from 1984, when the Minister granted exemption from the 25% requirement under the Banking Act. By June 1994, paid up capital stood at $15.75 million. All loans stood at $332 million, of which $57 million had been lent to only six customers. The rapid growth of the Bank was not a sign of success as White pointed out. He said; “Such growth is obtained by accepting business of dubious quality, particularly from customers who have been denied facilities by other institutions. Such growth places a burden on the institution’s monitoring capacity such that loan delinquency is unlikely to be checked at an early stage when the prospects of loan rehabilitation are still fair.”

What were other warning signs that all was not well, and which should have featured in audit advice and annual reports? Rapid growth when a significant number of senior staff had left the Bank and migrated or joined other banks, the lending to high risk borrowers without stringent lending requirements imposed by the Bank, the decision made by the Board to write off accumulated bad debts in 1994, apparently because of cyclone Oscar (making subsequent operating profits look healthier than they were), the failure to provide joint financial reports for the National Bank and its subsidiary the MBf (a limited liability company in which the NBF held 51% shares, and which dealt mainly in the credit card business) and therefore its failure to reflect the accumulated losses of MBf in its annual report, delays in the publication of the annual reports and the refusal to accept that the bank was unable to control its operations at least by 1993, were all warning signs. In 1993, the Auditor- General gave a qualified report on the Bank, mainly on the grounds that there was inadequate provisioning of bad debts and that the bank was particularly exposed to risk in relation to at least $57 million. Yet even in 1993, the Bank (and presumably its auditors) refused to accept that the Bank was insolvent. We cannot blame the 1987 coups or a culture of fear for the silence of the auditors before 1987, when the Bank was already heading for trouble. History is silent on what the internal auditors were telling the Financial Controller, the CEO and the Board of the Bank. Whatever they may or may not have said, one thing is demonstrably clear; the system of internal audit at the Bank was not working long before 1987.

What can we say of the external auditor, the Auditor-General? Should he have warned Parliament of the disaster that was the Bank, long before 1993?

The first criticism must be in relation to the delay in the publication of the audit reports. An institution in trouble will often delay a report of bad news for as long as possible. What we do not expect is for the Auditor-General’s Office to generate such delay. The report for the financial year ending 30 June 1988 was not released by the Auditor-General until June 1989. The audit report for the year ending June 1989 was released in February 1990. In 1993, when things were beginning to reach the public sphere, the audit report was delayed only by 6 months, and in 1996, by less than 3. By June 1994, the Auditor-General clearly had difficulties with the audit, “…qualifying the audit report on a number of issues, specifically the inadequate provisioning for bad debts, and the high risk exposure on six loans totalling $57 million. The NBF also received a qualified audit report for 1993, although the Bank contested this. This indicated that at this stage the bank’s operations were out of control. While this is demonstrably true, the NBF’s refusal to accept this in 1993 will have contributed to the audit difficulties to both the 1993 and 1994 reports.”

What is not clear is why the Auditor-General did not issue qualified reports prior to 1993. White suggests that this was because of repressive political conditions after 1997, but also asks why the Auditor-General did not point out risks before 1987, especially in relation to the Stinson-Pearce loans. He suggests that the public service was so badly governed that the standards of banking practice even before 198, were taken for granted and accepted as the norm. He also suggests that even if the Auditor had pointed out governance and banking risks, the Bank was not prepared to listen. Indeed, the 1993 report was met with an attack on the Auditor-General by the then Chairman of the Bank. The Chairman said that the audit report was “grossly unfair” and that the audit of the Bank should be given to an international firm and taken out of the hands of the Auditor-General!

However, criticism, refusal to give information, public insults and political attacks are all in a day’s work for the Auditor-General. He or she should be used to such response from the persons audited, and should factor in such opposition when conducting an audit. Just as accused persons are not expected to welcome being charged with criminal offences by the DPP, public officials are not expected to applaud audit accountability. Accountability is painful.

Detecting corruption in the public sector

I now move to public sector corruption. Corruption has now been redefined in the Crimes Decree and in the Bribery Promulgation. It now uses the word “bribery” rather than “corruption”, it reverses the burden of proof on the element “without lawful authority or reasonable excuse”, it creates a much wider definition of who is a public official by specifically including Ministers, judicial officers and contract service providers, and provides that a person can be bribed with any kind of benefit even if the benefit has no monetary value. Political gain can be a benefit for the purpose of the Crimes Decree. However the law has not always been tough on corruption. One of the greatest hurdles for the prosecution under the old Penal Code definition of corruption was the requirement that a bribe was given “on account of” an official act. In other words, the prosecution had to prove that a bribe was given in exchange for a specific official act or duty. If the act was in fact done by someone else, or by a board or committee, and there was no evidence that the official was instrumental in the doing of the act, there was no case. This hurdle failed to reflect how government departments work. Often a bribe to a Minister or a Permanent Secretary will achieve the result because these two people wield the real power in a Ministry. Internal committees and boards may be leaned on to do what the Minister or permanent secretary wants. It is a brave committee which decides contrary to their wishes. Thus a bribe may be given not to the committee, but to the Minister in order to influence a result from the committee.

The case of State v. Inoke Devo illustrates this. Inoke Devo was the Commissioner Central and in that capacity was a member of the Central Liquor Tribunal. The Tribunal was chaired by the Chief Magistrate. He was charged on four counts of corruption and four counts of abuse of office. Abuse of office is an offence which is closest to bad governance practised by a public servant. It requires proof that a person employed in the public service does or directs an act which is arbitrary and an abuse of office, and which is prejudicial to the rights of others. An arbitrary act has been defined as an unreasonable act which is not guided by rules and regulations but by the “whims and fancies of the doer”. It is a prosecutor’s favourite because it does not require proof that a benefit was given to the accused in return for the official act. Inoke Devo’s role in relation to liquor licenses was to issue and sign them after the Tribunal and police had vetted them and agreed to their being issued. The judge 14directed the assessors thus about the meaning of the word “corruptly”; “If I received money from an accused as an inducement to decide a case in favour of the accused in discharge of my official duty as a judge then I have done so corruptly. But if I have decided the case in favour of the accused based on the law and evidence and not that I have received any benefit from the accused, I have not acted corruptly.”

As a matter of law, this statement cannot be faulted. Under the Penal Code that was what the law was. In the case of Inoke Devo, the evidence was that he had received fish, liquor, and pig food from persons who had applied to the Tribunal for liquor licenses, and that they gave him these benefits “because the accused signs the liquor license(s)”. The evidence was that these gifts were known at least to the messenger who worked at the Commissioner Central’s office, the official driver at the office, and a secretary who processed the licenses and organised the office Christmas party. It was also known to the office accounts clerk, who presumably recorded the office accounts. His evidence was that he was asked to accompany the driver to collect the free liquor! The accused said that he did receive fish and some of the liquor, but denied sending the official car to collect liquor and pig food. However the crux of his defence was that he had not received any of these gifts in return for the issuing or renewing of licenses. He said that that decision was made by the tribunal and not by him. He was acquitted on that ground by the assessors and the judge. He was found guilty of abuse of office, but not of corruption.

An earlier case of official corruption, Prem Chand v State was symptomatic of all early corruption cases. It was about the prosecution of a medium level public servant who obtained a small amount of cash in return for a single act of corruption. In Prem Chand, the accused was a prison officer who obtained $100 for himself for altering the sentence of imprisonment recorded on a warrant of commitment. Such bribes were impossible to audit because there was never any record of them on the official records. The evidence was always dependent on the witness who gave the bribe. If the register of sentences and the original issued warrant tallied, who was to know if alterations had been made to the court copy? Later cases of small level official corruption highlight the same difficulty. In FICAC v. Rizvi the two accused were charged under the Prevention of Bribery Promulgation which has offences similar to the Crimes Decree corruption offences. The accused Rizvi was an importer of second hand car parts. He had imported a container load of spare parts which had to be examined by a customs officer. The accused Utovou was a customs officer, who opened the container, examined some spare parts, and then left after accepting $200 from Rizvi. When the matter was investigated by FICAC, the Fiji Islands Inland Revenue and Customs Authority re -evaluated the container and found that Rizvi had a liability of more than $1000 in custom duties on the container. The amount of the bribe was not considered a mitigating factor by the judge who imposed custodial sentences on both accused in addition to fines. The judge listed the betrayal of trust as a customs officer, and the harm done to the reputation of the public service to be the major aggravating factors for the second accused. The accused Rizvi was given a heavier sentence than the customs officer, the deciding factor being the financial gain to the importer.

Interesting as this case was, for the purpose of an auditor, how could the offence have been detected if FICAC had not discovered the corruption? In the absence of a whistle blower, it is very difficult to detect this kind of corruption. The examination of goods imported to Fiji requires careful documentation. However, that documentation is, of necessity, dependent on the information given to customs by the importer and the importer’s agent. Ships’ manifests, customs declaration forms and registers can only be verified by physical examination, much of which is not supervised. There is a real risk of collusion between the importer and customs officers. I am not for a minute suggesting that such collusion is widespread or systemic. I am saying however, that where the accuracy of audits depends on physical examination of goods and services, there is a risk of corruption and fraud. That risk can only be met by a good whistle blowing procedure which is anonymous, and an audit which requires physical spot checks. After all, the combination of both strategies exposed the Flour Mills fraud in the 1970’s in Fiji.

I now move on to larger corruptions. I call them larger, although the offences charged may not be for official corruption or bribery, because they involve the abuse of public power for private gain. In 1995, there were investigations into the affairs of the Housing Authority, the Fiji Development Bank, the Fiji Broadcasting Commission, the Fiji Public Service Credit Union, the Public Trustees Office, and the Methodist Church. In 1997, police were investigating alleged corruption and mismanagement in the Customs Department, the Housing Authority, the Companies Office and the Registrar- General’s Department. Prior to those investigations there were well publicised investigations into the Rewa Dairy Cooperative and the Hurricane Relief Fund. In none of these investigations were irregularities exposed by internal auditors. If they were, the auditors’ advice and recommendations were ignored and obscured by management.

A classic example is the fraud and corruption at the Housing Authority. In 1987, the Housing Authority was restructured, and the Lautoka office was made autonomous and virtually self-governing. We are here to identify corruption risks, and the Housing Authority was an example of the risks involved in allowing branch offices to function unsupervised and in disregard of company policy. A crucial requirement of governance is that there is an accountable system of internal surveillance, supervision and monitoring. The Lautoka office of the Housing Authority had launched major development projects for housing in Lautoka. A major contractor for building the houses and developing the project for the Housing Authority in the West was Raj Krishna Construction Company. The company also built houses for the business manager of the Housing Authority in the West, the General Manager Western and for the Chief Executive Officer of the Authority, Isikeli Kini. The relationship between the Authority and the company was described by the Lautoka Magistrates Court as “friendly and casual…..whereby jobs and contracts were awarded and favours returned in reciprocity.” No tenders were called for the project. No quotations were received. No estimates or costings were done before or after the awarding of contracts. The General Manager Western Epeli Naqase acted as administrator of the project and as a technical advisor. He and the business manager, Dharmend Kumar awarded certified and signed cheques, although invoices and supporting documents were twinked and altered, and although there was clear evidence of double invoicing, over payments, false quotations and forged tender minutes. The Auditor-General highlighted the discrepancies, and the Thompson Commission of Inquiry was set up to make recommendations. Eventually, there was a police investigation and ten persons were charged in relation to the case.

The charges were conspiracy to commit a felony, official corruption, abuse of office, conspiracy to commit a misdemeanour namely fraudulent falsification of accounts, and forgery. Charged were the CEO of the Housing Authority, Isikeli Kini, Radha Krishna Mudaliar, Epeli Naqase, Dharmend Kumar, and five other employees of the Housing Authority or the company. What was interesting was that the 8th accused was the accountant and tax agent for the company. The 7th accused was the accounts clerk at the Housing Authority. The case is an example of what can happen when the employees of an institution, including its accountants and auditors, conspire to defraud the organisation and ensure that internal accounts do not reflect the forgery. The defences at the trial for the company executives were that all work that was paid for was carried out, and that no free services had been given to Housing Authority staff. The defences of the Housing Authority staff were that there were loose or non existent procedures for tenders and payments, and that the Standard Tender Procedure for the Authority was not the only procedure followed in the awarding of tenders. However, tendered at the trial was a memorandum written by Isikeli Kini himself, which read as follows; “Attached herewith is a copy of the procedures for tender in respect of the sale and procurement of goods and services approved by the H.A Board. These procedures are self-explanatory and effective immediately.”

There was no dispute that these procedures were not followed, but there was also no doubt that the Housing Authority did not follow these procedures from 1994 to 1996 with the knowledge of senior management and accountants. It was not until 1997 that the Auditor-General discovered the fraud and corruption and brought it to the attention of the law enforcement agencies. The Auditor- General found evidence of the double invoicing, and the altered tender documents. There was other evidence of the fraud, but the case in court could not have succeeded without the evidence of the Clerk of Works who was instructed by his superiors to falsify costings, calculate costings from the contractors’ invoices without physical checks on sites, and to prepare costings after the work had already been done and paid for. Further, the police found evidence that was not available to the auditors; that the contractor had built houses, made loans, given cash and groceries, and paid for family funerals for the staff of the Housing Authority. There was evidence that the contractor built the private house of the CEO, charging him only $30,000 when the estimated cost of building it was in excess of $65,000.

During the duration of the fraud, no financial information was sent to Suva from the Lautoka office. The General Manager Finance had complained about it, but no action was taken because as the General Manager (the 3rd accused) said at the trial “the restructure gave the West autonomy and there was no need to send information”. The Board did not approve any of the expenditure because the Board knew nothing about it. Approvals for funding were given by the CEO, although the amounts approved were beyond his authority. Entries of expenditure were made under different heads to conceal the nature of the expenditure. All accused persons were found guilty as charged, and all were given custodial sentences ranging from 2 years to 9 months. No sentences were suspended. Appeals against convictions and sentences were dismissed. The court judgment is silent on the role of the internal auditors whilst the fraud was in operation at the Housing Authority. There is no doubt that some accounts staff were colluding in the fraud, and that some benefitted by gifts and favours given to them by the contractor. It cannot be denied, that no matter how good an accounting system is, a dishonest auditor can falsify and suppress accounts to give the impression of regularity. However the case is a good example of a system where warning signs of corruption should have been spotted very early in the day and certainly before the Auditor-General spotted problems two years later.

The case of Peniasi Kunatuba v State did not include charges of official corruption, but was about abuse of office for gain. The case falls into the wider definition of corruption. In that case although Cabinet, in 2000 had approved the Blueprint to advance the interests of the indigenous in Fiji, it had not allocated a budget for its implementation. The accused, the Permanent Secretary for Agriculture, decided to implement it by commencing a scheme to give 100% farming assistance to people, and by allowing payments to be made to a number of hardware merchants in Fiji. It was alleged that he abused his office, and that on one count, he did so for gain. He was convicted and his convictions were upheld on appeal by the Court of Appeal. In the course of evidence, the defence said that this was no scam, and was only a case of “creative accounting”. However the evidence showed examples of payments “made to suppliers without quotations or repeated quotations, no delivery dockets confirming supply, open and split LPO’s”.

The scheme continued over a period of 12 months and was finally the subject of investigations by the Ministry of Finance in August 2001. In the same month, the Scheme was finally referred to Cabinet in an attempt to get, what was in effect, retrospective approval. It was not forthcoming, and the Scheme was suspended. However in the Ministry’s response to the Auditor- General, who wanted to know why the Ministry had made unauthorised expenditure, reliance was made on the extraordinary circumstances which followed the 2000 coup. This was the response; “It is an exercise in futility to keep harping on the fact that the funds were unauthorized. Fiji was in abnormal circumstances and this called for abnormal solutions. As the CAO, Mr Kunatuba was only exercising his best judgment. That is why he had been appointed as the Permanent secretary of the Ministry. The situation called for vision and calculated risks. As CAO, in his judgment it was best not to keep to the modus operandi of normal times, and it would have been futile to do so. We submit though that the authority to utilize approved funds for the new programme was not sought. He and his management were working on the advice of his support staff.”

Perhaps the reason why the advice which came from the support staff was not dependable was that the Principal Accounts Officer, Suliasi Sorovakatini was himself involved in the scam. He, and the Managing Director of Suncourt Hardware Ltd, were charged with official corruption and found guilty of it. The Principal Accounts Officer was convicted of receiving benefits on account of approving payments in breach of government procedure. The benefits were free tickets to travel abroad, credit facilities at Suncourt Hardware, building materials and cash advances. Dhansukh Lal Bhikha the Managing Director of Suncourt was convicted on 3 counts of corruption for giving benefits to Sorovakatini. It is clear, that no matter how good the system of internal audit was at the Ministry, it was doomed to fail given the involvement of its Principal Accounts Officer in corrupt activities. The Agriculture Scam does highlight risk factors in cases of corruption.

Signs of corruption and fraud

Firstly; the existence of “abnormal circumstances”. Whether we experience a coup, or a flood, or a hurricane, there are many executives and accountants who appear to believe that such circumstances give a license to spend money without observing accounting procedures. In fact, because of the real risk of financial opportunism in such circumstances, shouldn’t internal controls be more severe, rather than less severe? At times of political instability, there must be stronger strategies to protect the purse of the public or the shareholders. Fiji’s history with fraud shows us that no such strategies exist.

Secondly; the relationship between government policy and corporate behaviour sometimes lacks clarity. It is government prerogative to have policies. However, in a government department, policies must be implemented within budgetary limits, and in accordance with the rules and regulations of the public service.

Thirdly, political neutrality in the civil service is mandatory. It is not for civil servants and statutory bodies to collect money for or to support any political party. Loyalty to government and active political lobbying are two distinct matters. The first is expected of civil servants, but the second is bad governance.

Fourthly, our traditional respect for authority and authority figures often prevent us from doing our duty with courage and integrity. Whether this comes from our upbringing, whether we are culturally programmed to respect those who hold positions of power even when we know they are breaking the law or procedure, or whether we remain silent because we do not want to lose our jobs, the result is a reluctance to blow the whistle on potentially corrupt and fraudulent activity. To that extent, audits will fail unless accountability has a degree of independence from persons who hold the most power in an organisation.

Fifthly, a close personal relationship between builders and public officers is very suspicious. The giving of gifts, the attendance at family birthday parties and funerals, the borrowing of money from the contractor and the unofficial meetings are all signs of attempts to influence a public officer to favour the financial interests of the contractor.

Sixthly, a contractor who has a contract with a government or statutory agency should not build houses or provide goods and services to employees of that department or agency. The temptation to give discounts, or provide free services is too great. I am not suggesting that all government employees should cease to shop at Vinod Patel or R. C. Manubhai when these private companies are awarded government contracts. What I am saying is that those officers who have a role in the awarding of contracts, or approving of payments, or the checking of invoices should refrain from personal transactions with those companies while engaged in these roles. If there is an overly close relationship, the warning signs exist for potential corruption and fraud.

Seventhly, some knowledge of forensic accounting is useful for auditors. Documents which are altered or twinked are a dead giveaway for fraud. They are often altered because the original does not match the payment made or due. Altered documents must have explanations – who altered them? When? Why? On what evidence? Double invoicing is also a dead giveaway. However to identify where it exists, the auditor must first understand the work to be done and the time within which it was to be done. Payment for the same roof twice in 6 months must start to ignite suspicions. In government service, the writing of Local Purchase Orders (and in banks the writing of foreign exchange transactions) which show amounts just below the limit allowed by law or procedure, is a common feature in fraud prosecutions. In the cases surrounding what we now call the Agriculture Scam, split LPO’s allowed the Ministry of Agriculture to spend a large proportion of $18 million without budgetary allocation or approval from the Ministry of Finance.

Eighthly, no branch office should be financially autonomous. Financial information should be given regularly to head offices and audits should be conducted from head office; not by auditors who sit in the branch office and who might be too close to the persons being audited.

Ninthly, budget approvals beyond the powers of management must be strictly scrutinised. The CEO is accountable to the Board. Yet many Boards behave as though the relationship were the other way around. I have said before, and will continue to say, that many boards suffer from one of two maladies, they are either hyperactive and interfere far too much with operational matters, or they are in a coma from which they only emerge in time to eat the annual Christmas lunch. Where a Board is either too weak or too strong, the recipe for corruption needs only one dishonest mind to complete it.

Lastly, delays in the release of audit reports encourage fraud and corruption because the delay has effectively put off the evil day of accountability.

There are many other cases which have come before the courts which illustrate the risk factors I have outlined. FICAC v Tevita Peni Mau and Mahendra Motibhai Patel a case of conflict of interest by the Chairman of the Post Fiji Board, and of the CEO who approved payment for a clock to be placed on the Post Office building without proper tender processes being followed and for an amount in excess of the CEO’s purchasing authority, FICAC v Anasa Vocea a case of a Permanent Secretary who failed to pay directors’ fees to the government and instead kept the money in an overseas bank account, and most recently, and on appeal, the case of FICAC v. Laisenia Qarase a case involving 6 counts of abuse of office and 3 counts of “discharge of duty with respect of property in which the accused had a private interest”, in relation to a director of Fijian Holdings buying company shares for his family owned and community owned companies.

These cases add little to the risk factors I have outlined. However, one thing is evident; that most companies and departments in Fiji do not have effective anonymous whistle blowing procedures to allow information on corruption without victimization, and that there is a real confusion amongst our citizens about what corruption is. Is it acceptable to show favouritism to one’s own clan in making appointments? When is a gift given by a client or customer a corrupt benefit received with an intention to be influenced? What is a corrupt benefit? If I receive $500, but I am not the person who will make the official decision, am I corrupt? If I break all the rules in order to make a profit for the shareholders, am I a crook or a hero?

A Summary of Corruption Risks

If I were to list a number of risk scenarios for corruption in Fiji, I would list them as follows;

1. Internal auditors who lack objectivity in relation to management or are themselves involved in fraud;

2. Boards of Directors which are either over active or too reliant on management and cannot question management decisions;

3. Political instability and natural disasters which may lead to loose accounting practices;

4. Lack of knowledge of forensic accounting and delay in the issuing of audit reports;

5. A lack of neutrality in relation to government policies in the civil service;

6. Cultural and management authority which prevents auditors from being forthright in their opinions;

7. Branch autonomy;

8. Exceeding purchasing limits without Board approval;

9. Undeclared conflicts of interest;

10. Unhealthily close relationships between tenderers and tenderees and vague policies on the receiving of gifts and corporate hospitality;

11. No whistle blowing procedure which is anonymous and includes a guarantee of non-victimization;

12. Too much discretion without adequate supervision on licensing, building and regulatory duties;

13. Mixed and confusing messages to staff from management about tolerance of corruption related activities;

14. Tender procedures which lack uniformity and transparency and which are tailored to grant contracts to a pre determined person or company;

15. Tender proposals which are deliberately tailored to be lower than all others but which are far lower than the actual total cost of building will be.

And, for the Auditor- General’s Office in particular, I would add the additional risks;

16. Political interference and political and bureaucratic pressure on the Office to conform to the “party line”;

17. Attempts to use the public service bureaucracy to restrict the Auditor’s ability to be independent and to demand information from those who are audited;

18. A lack of statutory protection from other government agencies;

19. The silence of those who are too frightened of losing their jobs, to speak the truth;

20. The failure of government agencies to have anonymous whistle-blowing procedures;

21. A misplaced sense of loyalty to the boss. Employees owe loyalty to the institution, not to individuals.

The New Law on Corruption.

The Crimes Decree definition of corruption is significantly different from the Penal Code definition of official corruption. Section 135 of the Crimes Decree (called “Receiving a Bribe”) reads as follows;

“(1) A public official commits an indictable offence (which is triable summarily) if –

(a) the public official without lawful authority or reasonable excuse –

(i) asks for a benefit for himself, herself, or another person;

(ii) receives or obtains a benefit for himself, herself or another person;

(iii) agrees to receive or obtain a benefit for himself, herself or another person; and

(b) the public official does so with the intention-

(i) that the exercise of the official’s duties as a public official will be influenced; or

(ii) of inducing, fostering or sustaining a belief that the exercise of the official’s duties as a public official will be influenced.”

What has changed? Firstly, the words “on account of”’ no longer feature in this definition. This means that the prosecution no longer has to prove a necessary nexus between the benefit and a specific official act. Secondly, the fault element in the new offence is “with the intention of being influenced as a public official” so that influence in the broader and more realistic sense is all that is necessary for proof. Thirdly the words “without lawful authority or reasonable excuse” create a negative averment, placing the burden of proving that there was a reasonable excuse or lawful authority on the defence, to prove on a balance of probabilities. This shift has been held by the Privy Council,30 considering a similar provision in the Hong Kong legislation, to be in accordance with the right to a fair trial. Lastly, the word “benefit” now specifically includes political advantage and is not restricted to things with a monetary value.

All of this makes corruption easier to prosecute. However the law cannot persuade auditors to be more discerning and more forthright. Nor can it persuade whistle blowers to blow the whistle. The investigation of corruption is still as challenging as it was. The law can only make the prosecution easier if the investigators have obtained evidence, and if there are witnesses who are willing to give evidence.

Conclusion

The role of the Auditor-General has been important in Fiji’s history of fraud and corruption. He blew the whistle in the National Bank, the Housing Authority, and in the Agriculture scam, when no one else was prepared to criticise the downward spiral in the financial affairs of public offices. However, the Office can only succeed in effectively blowing the whistle on fraud and corruption, if its auditors are able to detect the first signs of trouble, and if they are able to work freely without political pressure or fear. Administrative control is sometimes a cover for institutional control. The institutional strength of the Office is crucial to Fiji’s future. Edited version; see full below:

Fijileaks Editor: The chair of NBF was none other then Winston Thompson, still serving as Fiji's Ambassador to Washington.

The FNPF saga and the ghost of the collapsed National Bank of Fiji scandal, Part One of a Special Report by VICTOR LAL: http://www.coup5.com/2010/05/fnpf-saga-and-ghost-of-collapsed.html

Address to the Office of the Auditor-General, Fiji

By Nazhat Shameem

5th December 2012

"An institution in trouble will often delay a report of bad news for as long as possible."

Since the parlous state of the bank’s finances became known to the public, there has been a tendency to view the auditor-general as the saviour of the public because it was the qualified audit of the NBF that finally brought the bank’s problems into the open. Yet the fact remained that when the auditor-general ‘blew the whistle’ on the NBF, he blew too softly and too belatedly. It is worth noting that over the 1991 to 1995 period the NBF’s situation was studied frequently by the Reserve Bank. This also raises a crucial issue of cooperation between the Reserve Bank and the auditor-general. What is not in the public record is whether the auditor-general was aware that the NBF was deemed insolvent by the Reserve Bank and whether the Reserve Bank had fully disclosed information about the NBF to the auditor-general.”

Introduction

At the time the National Bank was investigated by the Reserve Bank of Fiji and the Fiji Police Force for possible fraud and corruption, I was the Director of Public Prosecutions. I, the Auditor-General, the Supervisor of Elections, the Commissioner of Police and the Ombudsman were the constitutional officers appointed under the 1990 or 1997 Constitutions and entrusted to hold society to account for abuses of power and public money, or entrusted to protect free elections and human rights. As the NBF investigations gained momentum, so did attempts by the executive to control the constitutional officers. There were attempts to make us accountable to various permanent secretaries in our “performance”, and when we refused, attempts to amend the 1997 Constitution to write in such accountability. Fortunately, the Constitution could not be amended without the support of the Opposition. Such support was refused, and the performance agreements were never signed.

However, the incident reminded me of the importance of the independence of the office of the auditor-general in relation to government bureaucracy. At this time, when Fiji is working towards a new constitutional framework, it is important to remind ourselves that institutional independence in offices designed to hold others accountable, must be strengthened, not weakened, and that the most effective way to undermine the effectiveness of offices such as the Auditor-General’s is to create a bureaucratic form of control over the performance of the auditors. A strong Auditor-General is a most important guard against bad governance. Sadly, Fiji has had a shocking history of bad governance, with risk factors which are specific to Fiji’s business climate and political history.

Our fraud history

We cannot blame the auditors for fraud or corruption. However, the failure to detect fraud and corruption, and the failure to identify the signposts for corruption risks, is a failure of the auditor. How this may manifest itself is sometimes problematic.

In a recent case in the Lautoka High Court Sunbeach Fiji Limited, the company which owns the Trans International Hotel in Nadi brought an action in negligence against its external auditors for failing to detect a fraud of $83,756.11. The action is still pending. The statement of claim alleges that the audits of the two preceding years should have uncovered the fraud. However the auditors said in response that they did highlight weaknesses in the accounting practices of the company in their 2009 and 2010 reports. The reports spoke of internal control procedures which were weak, and of the possibility of potential fraud. The auditors found missing receipt books, missing food and beverage dockets, and a missing front office guest ledger and other weaknesses which indicated a “chronic poor accounting management system at Sunbeach”. However Sunbeach said that simple bank reconciliations would have shown that what should have been in the bank according to the hotel’s accounts, and what was in fact in the bank account for the bank did not correspond. All of this led to an acrimonious exchange of emails between the hotel and Ernst and Young, and finally to the refusal of the auditors to lodge the company’s tax returns, on the grounds that the returns should not have contained accounts signed off by the company when it knew that there had been a fraud on the accounts. The matter went before the Master for discovery of all audit documents in relation to the hotel by the accountants to the hotel. The Master refused the application, calling it a “cleverly disguised fishing expedition” and expressing the view that the plaintiff had no case against the accountants in any event because it had failed to produce evidence that there was indeed a fraud.

Although the case is still pending, it does illustrate the possible disconnection between what auditors think they are supposed to detect, and what their clients think they are supposed to detect. It also illustrates that (in that case the external auditors) auditors are often in the front line for the detection of fraud and corruption, and must learn to recognise the corruption and fraud signposts in order to report accurately to the clients. The first major fraud to be detected in Fiji was the Flour Mills case. That was a case of a company which had special agreements with government to mill enough flour for local consumption in return for exemption from customs duties and ports fees. When the company started to make a significant profit, the Board was afraid that these concessions would be withdrawn by government, and asked the management to falsify the amount of profits and stock the company had, in order to conceal the true state of affairs. This was a criminal offence, and the Financial Controller blew the whistle on the company by writing to the then Prime Minister. The Prime Minister asked an independent auditor to conduct an audit, and the audit commenced with the simplest test of all; an examination of how much wheat was in fact in the silos of the Flour Mills of Fiji. A prosecution followed and led to convictions. However, an appeal against the convictions succeeded, and no retrial was ever conducted.

The National Bank of Fiji was the next major financial scam. Said to have commenced from 1978 to 1985 when the Minister of Finance approved the exemption of the Bank from the rule in the Banking Act that no one customer should be lent more than 25% of a bank’s equity, by 1996 the Bank was owed about $220 million, over 8.5% of GNP. The rot commenced long before the 1987 coup, but events after 1987 lurched from one banking disaster to another. The Bank seemed to be confused about its real role. Was it a development bank, created to implement social justice, or was it a commercial bank? It followed reckless lending policies, ignored internal procedures and sound banking practices and grew rapidly when it lacked the ability to manage such growth. During this reckless history, there was a resounding silence from the internal auditors of the Bank.

So insignificant was the role of internal auditors in the case of the National Bank of Fiji, that it has never got a mention in any of the analyses of the Bank’s collapse. In “Crisis; The Collapse of the National Bank of Fiji” there is much discussion on the role of the Reserve Bank in its failure to stop the bank operating after it was technically insolvent, and on the role of the Auditor-General (who blew the whistle too softly and too late) but not of the role of the internal auditors. Yet the internal auditors must have been instrumental in providing reassuring reports to the Board of Directors that all was well in the State of Denmark. Is it possible that they did not know what was happening? After all, according to Grynberg, Munro and White, “on paper there were more than sufficient safeguards”. In fact, the internal audits could not have missed the widespread disregard for prudent banking procedure, the dishonesty, the loans approved on the telephones and bits of paper, and the inadequate or missing securities. Did they report the irregularities? The lending without adequate securities? The use of patronage to approve loans? We will never know. However from the Auditor- General’s reports, and from the Annual Corporate Reports of the bank, one is able to draw some conclusions about the role of the auditors and accountants in the collapse of the Bank. Michael White said this of audit reports generally; “The accounting profession has come under sustained attack over a long period for its apparent inability to identify imminent corporate collapses through the legally acquired annual corporate reports. A substantial literature points to many examples of organisations reporting profits and a generally solid financial position, applying generally accepted accounting practices, receiving an unqualified audit report, yet proving bankrupt within twelve months of the reporting date.”

We do not know what the internal auditors told their superiors at the Bank but the annual corporate reports failed to mention that the Minister of Finance had given exemption to the Bank from the requirement under the Banking Act that aggregate loans to one customer should not exceed 25% of the bank’s equity. The annual reports showed that the Bank experienced rapid growth from 1984, when the Minister granted exemption from the 25% requirement under the Banking Act. By June 1994, paid up capital stood at $15.75 million. All loans stood at $332 million, of which $57 million had been lent to only six customers. The rapid growth of the Bank was not a sign of success as White pointed out. He said; “Such growth is obtained by accepting business of dubious quality, particularly from customers who have been denied facilities by other institutions. Such growth places a burden on the institution’s monitoring capacity such that loan delinquency is unlikely to be checked at an early stage when the prospects of loan rehabilitation are still fair.”

What were other warning signs that all was not well, and which should have featured in audit advice and annual reports? Rapid growth when a significant number of senior staff had left the Bank and migrated or joined other banks, the lending to high risk borrowers without stringent lending requirements imposed by the Bank, the decision made by the Board to write off accumulated bad debts in 1994, apparently because of cyclone Oscar (making subsequent operating profits look healthier than they were), the failure to provide joint financial reports for the National Bank and its subsidiary the MBf (a limited liability company in which the NBF held 51% shares, and which dealt mainly in the credit card business) and therefore its failure to reflect the accumulated losses of MBf in its annual report, delays in the publication of the annual reports and the refusal to accept that the bank was unable to control its operations at least by 1993, were all warning signs. In 1993, the Auditor- General gave a qualified report on the Bank, mainly on the grounds that there was inadequate provisioning of bad debts and that the bank was particularly exposed to risk in relation to at least $57 million. Yet even in 1993, the Bank (and presumably its auditors) refused to accept that the Bank was insolvent. We cannot blame the 1987 coups or a culture of fear for the silence of the auditors before 1987, when the Bank was already heading for trouble. History is silent on what the internal auditors were telling the Financial Controller, the CEO and the Board of the Bank. Whatever they may or may not have said, one thing is demonstrably clear; the system of internal audit at the Bank was not working long before 1987.

What can we say of the external auditor, the Auditor-General? Should he have warned Parliament of the disaster that was the Bank, long before 1993?

The first criticism must be in relation to the delay in the publication of the audit reports. An institution in trouble will often delay a report of bad news for as long as possible. What we do not expect is for the Auditor-General’s Office to generate such delay. The report for the financial year ending 30 June 1988 was not released by the Auditor-General until June 1989. The audit report for the year ending June 1989 was released in February 1990. In 1993, when things were beginning to reach the public sphere, the audit report was delayed only by 6 months, and in 1996, by less than 3. By June 1994, the Auditor-General clearly had difficulties with the audit, “…qualifying the audit report on a number of issues, specifically the inadequate provisioning for bad debts, and the high risk exposure on six loans totalling $57 million. The NBF also received a qualified audit report for 1993, although the Bank contested this. This indicated that at this stage the bank’s operations were out of control. While this is demonstrably true, the NBF’s refusal to accept this in 1993 will have contributed to the audit difficulties to both the 1993 and 1994 reports.”

What is not clear is why the Auditor-General did not issue qualified reports prior to 1993. White suggests that this was because of repressive political conditions after 1997, but also asks why the Auditor-General did not point out risks before 1987, especially in relation to the Stinson-Pearce loans. He suggests that the public service was so badly governed that the standards of banking practice even before 198, were taken for granted and accepted as the norm. He also suggests that even if the Auditor had pointed out governance and banking risks, the Bank was not prepared to listen. Indeed, the 1993 report was met with an attack on the Auditor-General by the then Chairman of the Bank. The Chairman said that the audit report was “grossly unfair” and that the audit of the Bank should be given to an international firm and taken out of the hands of the Auditor-General!

However, criticism, refusal to give information, public insults and political attacks are all in a day’s work for the Auditor-General. He or she should be used to such response from the persons audited, and should factor in such opposition when conducting an audit. Just as accused persons are not expected to welcome being charged with criminal offences by the DPP, public officials are not expected to applaud audit accountability. Accountability is painful.

Detecting corruption in the public sector

I now move to public sector corruption. Corruption has now been redefined in the Crimes Decree and in the Bribery Promulgation. It now uses the word “bribery” rather than “corruption”, it reverses the burden of proof on the element “without lawful authority or reasonable excuse”, it creates a much wider definition of who is a public official by specifically including Ministers, judicial officers and contract service providers, and provides that a person can be bribed with any kind of benefit even if the benefit has no monetary value. Political gain can be a benefit for the purpose of the Crimes Decree. However the law has not always been tough on corruption. One of the greatest hurdles for the prosecution under the old Penal Code definition of corruption was the requirement that a bribe was given “on account of” an official act. In other words, the prosecution had to prove that a bribe was given in exchange for a specific official act or duty. If the act was in fact done by someone else, or by a board or committee, and there was no evidence that the official was instrumental in the doing of the act, there was no case. This hurdle failed to reflect how government departments work. Often a bribe to a Minister or a Permanent Secretary will achieve the result because these two people wield the real power in a Ministry. Internal committees and boards may be leaned on to do what the Minister or permanent secretary wants. It is a brave committee which decides contrary to their wishes. Thus a bribe may be given not to the committee, but to the Minister in order to influence a result from the committee.

The case of State v. Inoke Devo illustrates this. Inoke Devo was the Commissioner Central and in that capacity was a member of the Central Liquor Tribunal. The Tribunal was chaired by the Chief Magistrate. He was charged on four counts of corruption and four counts of abuse of office. Abuse of office is an offence which is closest to bad governance practised by a public servant. It requires proof that a person employed in the public service does or directs an act which is arbitrary and an abuse of office, and which is prejudicial to the rights of others. An arbitrary act has been defined as an unreasonable act which is not guided by rules and regulations but by the “whims and fancies of the doer”. It is a prosecutor’s favourite because it does not require proof that a benefit was given to the accused in return for the official act. Inoke Devo’s role in relation to liquor licenses was to issue and sign them after the Tribunal and police had vetted them and agreed to their being issued. The judge 14directed the assessors thus about the meaning of the word “corruptly”; “If I received money from an accused as an inducement to decide a case in favour of the accused in discharge of my official duty as a judge then I have done so corruptly. But if I have decided the case in favour of the accused based on the law and evidence and not that I have received any benefit from the accused, I have not acted corruptly.”

As a matter of law, this statement cannot be faulted. Under the Penal Code that was what the law was. In the case of Inoke Devo, the evidence was that he had received fish, liquor, and pig food from persons who had applied to the Tribunal for liquor licenses, and that they gave him these benefits “because the accused signs the liquor license(s)”. The evidence was that these gifts were known at least to the messenger who worked at the Commissioner Central’s office, the official driver at the office, and a secretary who processed the licenses and organised the office Christmas party. It was also known to the office accounts clerk, who presumably recorded the office accounts. His evidence was that he was asked to accompany the driver to collect the free liquor! The accused said that he did receive fish and some of the liquor, but denied sending the official car to collect liquor and pig food. However the crux of his defence was that he had not received any of these gifts in return for the issuing or renewing of licenses. He said that that decision was made by the tribunal and not by him. He was acquitted on that ground by the assessors and the judge. He was found guilty of abuse of office, but not of corruption.

An earlier case of official corruption, Prem Chand v State was symptomatic of all early corruption cases. It was about the prosecution of a medium level public servant who obtained a small amount of cash in return for a single act of corruption. In Prem Chand, the accused was a prison officer who obtained $100 for himself for altering the sentence of imprisonment recorded on a warrant of commitment. Such bribes were impossible to audit because there was never any record of them on the official records. The evidence was always dependent on the witness who gave the bribe. If the register of sentences and the original issued warrant tallied, who was to know if alterations had been made to the court copy? Later cases of small level official corruption highlight the same difficulty. In FICAC v. Rizvi the two accused were charged under the Prevention of Bribery Promulgation which has offences similar to the Crimes Decree corruption offences. The accused Rizvi was an importer of second hand car parts. He had imported a container load of spare parts which had to be examined by a customs officer. The accused Utovou was a customs officer, who opened the container, examined some spare parts, and then left after accepting $200 from Rizvi. When the matter was investigated by FICAC, the Fiji Islands Inland Revenue and Customs Authority re -evaluated the container and found that Rizvi had a liability of more than $1000 in custom duties on the container. The amount of the bribe was not considered a mitigating factor by the judge who imposed custodial sentences on both accused in addition to fines. The judge listed the betrayal of trust as a customs officer, and the harm done to the reputation of the public service to be the major aggravating factors for the second accused. The accused Rizvi was given a heavier sentence than the customs officer, the deciding factor being the financial gain to the importer.

Interesting as this case was, for the purpose of an auditor, how could the offence have been detected if FICAC had not discovered the corruption? In the absence of a whistle blower, it is very difficult to detect this kind of corruption. The examination of goods imported to Fiji requires careful documentation. However, that documentation is, of necessity, dependent on the information given to customs by the importer and the importer’s agent. Ships’ manifests, customs declaration forms and registers can only be verified by physical examination, much of which is not supervised. There is a real risk of collusion between the importer and customs officers. I am not for a minute suggesting that such collusion is widespread or systemic. I am saying however, that where the accuracy of audits depends on physical examination of goods and services, there is a risk of corruption and fraud. That risk can only be met by a good whistle blowing procedure which is anonymous, and an audit which requires physical spot checks. After all, the combination of both strategies exposed the Flour Mills fraud in the 1970’s in Fiji.

I now move on to larger corruptions. I call them larger, although the offences charged may not be for official corruption or bribery, because they involve the abuse of public power for private gain. In 1995, there were investigations into the affairs of the Housing Authority, the Fiji Development Bank, the Fiji Broadcasting Commission, the Fiji Public Service Credit Union, the Public Trustees Office, and the Methodist Church. In 1997, police were investigating alleged corruption and mismanagement in the Customs Department, the Housing Authority, the Companies Office and the Registrar- General’s Department. Prior to those investigations there were well publicised investigations into the Rewa Dairy Cooperative and the Hurricane Relief Fund. In none of these investigations were irregularities exposed by internal auditors. If they were, the auditors’ advice and recommendations were ignored and obscured by management.

A classic example is the fraud and corruption at the Housing Authority. In 1987, the Housing Authority was restructured, and the Lautoka office was made autonomous and virtually self-governing. We are here to identify corruption risks, and the Housing Authority was an example of the risks involved in allowing branch offices to function unsupervised and in disregard of company policy. A crucial requirement of governance is that there is an accountable system of internal surveillance, supervision and monitoring. The Lautoka office of the Housing Authority had launched major development projects for housing in Lautoka. A major contractor for building the houses and developing the project for the Housing Authority in the West was Raj Krishna Construction Company. The company also built houses for the business manager of the Housing Authority in the West, the General Manager Western and for the Chief Executive Officer of the Authority, Isikeli Kini. The relationship between the Authority and the company was described by the Lautoka Magistrates Court as “friendly and casual…..whereby jobs and contracts were awarded and favours returned in reciprocity.” No tenders were called for the project. No quotations were received. No estimates or costings were done before or after the awarding of contracts. The General Manager Western Epeli Naqase acted as administrator of the project and as a technical advisor. He and the business manager, Dharmend Kumar awarded certified and signed cheques, although invoices and supporting documents were twinked and altered, and although there was clear evidence of double invoicing, over payments, false quotations and forged tender minutes. The Auditor-General highlighted the discrepancies, and the Thompson Commission of Inquiry was set up to make recommendations. Eventually, there was a police investigation and ten persons were charged in relation to the case.

The charges were conspiracy to commit a felony, official corruption, abuse of office, conspiracy to commit a misdemeanour namely fraudulent falsification of accounts, and forgery. Charged were the CEO of the Housing Authority, Isikeli Kini, Radha Krishna Mudaliar, Epeli Naqase, Dharmend Kumar, and five other employees of the Housing Authority or the company. What was interesting was that the 8th accused was the accountant and tax agent for the company. The 7th accused was the accounts clerk at the Housing Authority. The case is an example of what can happen when the employees of an institution, including its accountants and auditors, conspire to defraud the organisation and ensure that internal accounts do not reflect the forgery. The defences at the trial for the company executives were that all work that was paid for was carried out, and that no free services had been given to Housing Authority staff. The defences of the Housing Authority staff were that there were loose or non existent procedures for tenders and payments, and that the Standard Tender Procedure for the Authority was not the only procedure followed in the awarding of tenders. However, tendered at the trial was a memorandum written by Isikeli Kini himself, which read as follows; “Attached herewith is a copy of the procedures for tender in respect of the sale and procurement of goods and services approved by the H.A Board. These procedures are self-explanatory and effective immediately.”

There was no dispute that these procedures were not followed, but there was also no doubt that the Housing Authority did not follow these procedures from 1994 to 1996 with the knowledge of senior management and accountants. It was not until 1997 that the Auditor-General discovered the fraud and corruption and brought it to the attention of the law enforcement agencies. The Auditor- General found evidence of the double invoicing, and the altered tender documents. There was other evidence of the fraud, but the case in court could not have succeeded without the evidence of the Clerk of Works who was instructed by his superiors to falsify costings, calculate costings from the contractors’ invoices without physical checks on sites, and to prepare costings after the work had already been done and paid for. Further, the police found evidence that was not available to the auditors; that the contractor had built houses, made loans, given cash and groceries, and paid for family funerals for the staff of the Housing Authority. There was evidence that the contractor built the private house of the CEO, charging him only $30,000 when the estimated cost of building it was in excess of $65,000.

During the duration of the fraud, no financial information was sent to Suva from the Lautoka office. The General Manager Finance had complained about it, but no action was taken because as the General Manager (the 3rd accused) said at the trial “the restructure gave the West autonomy and there was no need to send information”. The Board did not approve any of the expenditure because the Board knew nothing about it. Approvals for funding were given by the CEO, although the amounts approved were beyond his authority. Entries of expenditure were made under different heads to conceal the nature of the expenditure. All accused persons were found guilty as charged, and all were given custodial sentences ranging from 2 years to 9 months. No sentences were suspended. Appeals against convictions and sentences were dismissed. The court judgment is silent on the role of the internal auditors whilst the fraud was in operation at the Housing Authority. There is no doubt that some accounts staff were colluding in the fraud, and that some benefitted by gifts and favours given to them by the contractor. It cannot be denied, that no matter how good an accounting system is, a dishonest auditor can falsify and suppress accounts to give the impression of regularity. However the case is a good example of a system where warning signs of corruption should have been spotted very early in the day and certainly before the Auditor-General spotted problems two years later.

The case of Peniasi Kunatuba v State did not include charges of official corruption, but was about abuse of office for gain. The case falls into the wider definition of corruption. In that case although Cabinet, in 2000 had approved the Blueprint to advance the interests of the indigenous in Fiji, it had not allocated a budget for its implementation. The accused, the Permanent Secretary for Agriculture, decided to implement it by commencing a scheme to give 100% farming assistance to people, and by allowing payments to be made to a number of hardware merchants in Fiji. It was alleged that he abused his office, and that on one count, he did so for gain. He was convicted and his convictions were upheld on appeal by the Court of Appeal. In the course of evidence, the defence said that this was no scam, and was only a case of “creative accounting”. However the evidence showed examples of payments “made to suppliers without quotations or repeated quotations, no delivery dockets confirming supply, open and split LPO’s”.

The scheme continued over a period of 12 months and was finally the subject of investigations by the Ministry of Finance in August 2001. In the same month, the Scheme was finally referred to Cabinet in an attempt to get, what was in effect, retrospective approval. It was not forthcoming, and the Scheme was suspended. However in the Ministry’s response to the Auditor- General, who wanted to know why the Ministry had made unauthorised expenditure, reliance was made on the extraordinary circumstances which followed the 2000 coup. This was the response; “It is an exercise in futility to keep harping on the fact that the funds were unauthorized. Fiji was in abnormal circumstances and this called for abnormal solutions. As the CAO, Mr Kunatuba was only exercising his best judgment. That is why he had been appointed as the Permanent secretary of the Ministry. The situation called for vision and calculated risks. As CAO, in his judgment it was best not to keep to the modus operandi of normal times, and it would have been futile to do so. We submit though that the authority to utilize approved funds for the new programme was not sought. He and his management were working on the advice of his support staff.”