Fijileaks Acting Editor, CJR: We are doing our best to clear a backlog of draft stories in our master system, including Victor Lal's reflective piece on the late Chief Justice Sir Timoci Tuivaqa. The late CJ was instrumental, backed by judges Daniel Fatiaki and Michael Scott, in providing judicial recognition of the George Speight terrorism by advising the late Ratu Mara to terminate Mahendra Chaudhry. They saw an opportunity to get rid of an Indo-Fijian Prime Minister!

'Speaking ill of the dead'? No, says Fijileaks

|  |

Rajendra Chaudhry responding to Victor Lal opinion column: "This matter has been answered before on numerous occasions. I have never had nor do I have any criminal record in Fiji nor anywhere else. I had a couple of traffic matters and these did not constitute criminal offences at any relevant time and certainly wasn't a disqualification from appointment to the civil service offence like Francis Kean. My appointment was made late August 1999 after medical and police checks but backdated to May 19, 1999 by the PSC. Vatuloka was obviously ill advised." 8 January 2016.

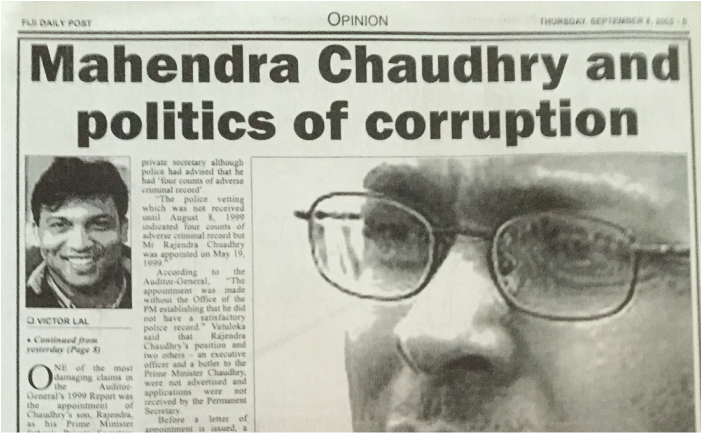

VICTOR LAL's Opinion piece 'Mahendra Chaudhry and politics of corruption', in Fiji's Daily Post, 2005, Excerpts:

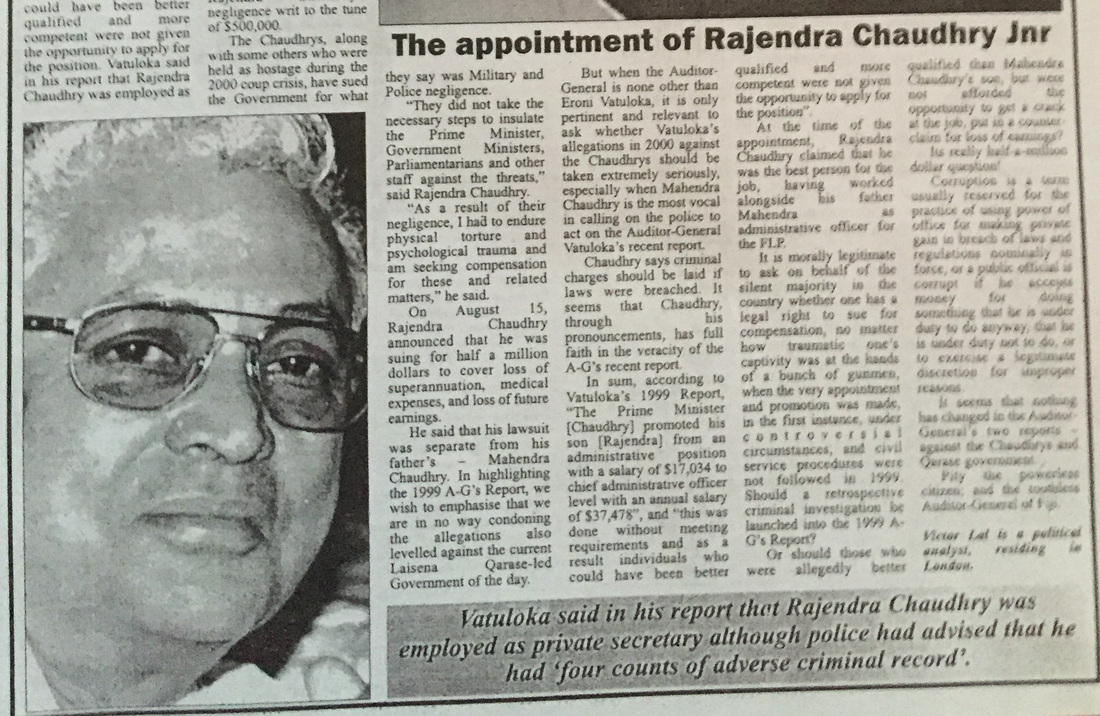

"ONE of the most damaging claims in the Auditor-General's 1999 Report was the appointment of Chaudhry's son, Rajendra, as his Prime Minister father's Private Secretary without following procedures. He [Rajendra] did not undergo a medical examination nor did he produce a satisfactory police record before he took the job on 19 May 1999. 'The Prime Minister promoted his son from an administrative position with a salary of $17,034 to chief administrative officer with an annual salary of $37,478,' the Auditor-General Eroni Vatuloka highlighted. [He] said this was done without meeting requirements and as a result individuals who could have been better qualified and more competent were not given the opportunity to apply for the position.

Vatuloka said in his report that Rajendra Chaudhry was employed as private secretary although police had advised that he had 'four counts of adverse criminal record'. 'The police vetting which was not received until August 8, 1999 indicated four counts of adverse criminal record but Mr Rajendra Chaudhry was appointed on May 19, 1999. According to the Auditor: 'The appointment was made without the Office of the PM establishing that he did not have a satisfactory police record'. Vatuloka said that Rajendra Chaudhry's position and two others - an executive officer and a butler to the Prime Minister Chaudhry were not advertised and applications were not received by the Permanent Secretary...Significantly, the Chaudhrys robustly defended themselves and refuted all allegations contained in the Auditor-General's Report, and now the taxpayers might be called upon to foot Rajendra Chaudhry's negligence writ to the tune of $500,000.

'As a result of their negligence, I had to endure physical torture and psychological trauma and am seeking compensation for these and related matters,' he said. On August 15, Rajendra Chaudhry announced that he was suing for half a million dollars to cover loss of superannuation, medical expenses, and loss of future earnings.

It is morally legitimate to ask on behalf of the silent majority in the country whether one has a legal right to sue for compensation, no matter how traumatic one's captivity was at the hands of a bunch of gunmen, when the very appointment and promotion was made, in the first instance, under controversial circumstances and civil service procedures were not followed in 1999. Should a retrospective criminal investigation be launched into the 1999 A-G's Report?

Or should those who were better qualified than Mahendra Chaudhry's son but were not afforded the opportunity to get a crack at the job put a counter-claim for loss of earnings? Its really half-a-million dollar question? Corruption is a term usually reserved for the office of making private gain in breach of laws and regulations nominally in force...It seems that nothing has changed in the Auditor-General's two reports - against the Chaudhrys and the Qarase government. Pity the powerless citizens, and the toothless Auditor-General of Fiji"

Fiji law firm was forcibly shut down (above)  The Ghost of 2000 laid to rest: Rajendra Chaudhry recently opened a new legal office in Auckland, New Zealand and has one in Australia |  2000: George Speight parades his captive prisoner Chaudhry  Rajendra Chaudhry and Anand Singh who defended Mahendra Chaudhry during the tax trial |

Proud Achievement: Mahendra Chaudhry catches up with New Zealand residents in Rajendra's new Auckland law office recently

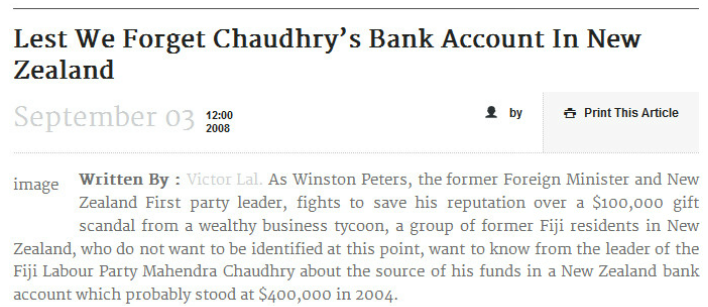

"On 26 September 2000, [Mahendra Chaudhry] had opened an account with ANZ bank in NZ, three months after he was released by George Speight from Parliament. On 1 June 2004, a month after FIRCA began closing in on him, he wrote to the bank requesting interest earned on his account number 981000000116059. On 16 July, the ANZ bank wrote to him detailing interest he received on the above account between 26 March 2001 and 26 September 2003. Chaudhry received interest income of $NZ23,274.47 or $F24,575.76. The exact amount of funds Chaudhry had in the bank there is not known, but according to forensic accountants, working backwards from the interest he received it was probably $300,000 to $400,000, raising the question of the original source of the New Zealand funds." - Victor Lal, 3 September 2008

From Fiji Sun archive, 3 September 2008, by VICTOR LAL

There is hardly any discussion or information about Chaudhry’s bank account in New Zealand, with the three-member inquiry team into his tax affairs, concluding as follows: “As noted above, FIRCA’s file does not disclose how they concluded that the monies invested into the New Zealand term deposit in September 2000 were non-taxable, although the committee notes that those funds were invested soon after the events of May 2000, which led to Mr Chaudhry ceasing to be Prime Minister of Fiji and very close to the times at which the deposits into the Australian account were made.In any event, the amount invested into the New Zealand account was small (less than 8 per cent of the total funds invested in the Australian and New Zealand accounts).”

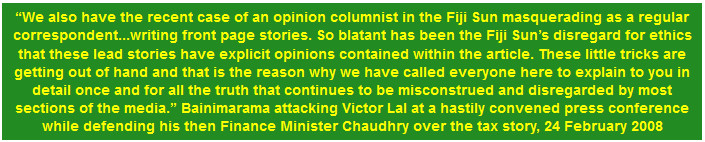

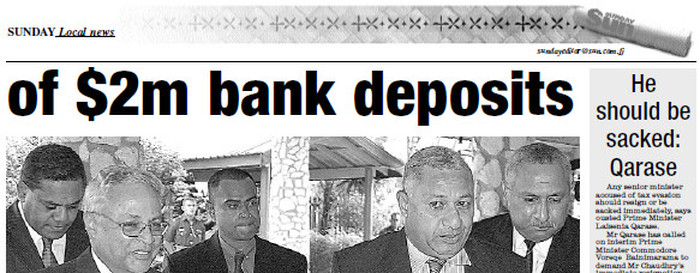

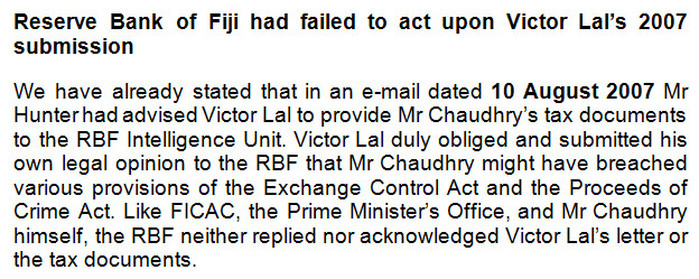

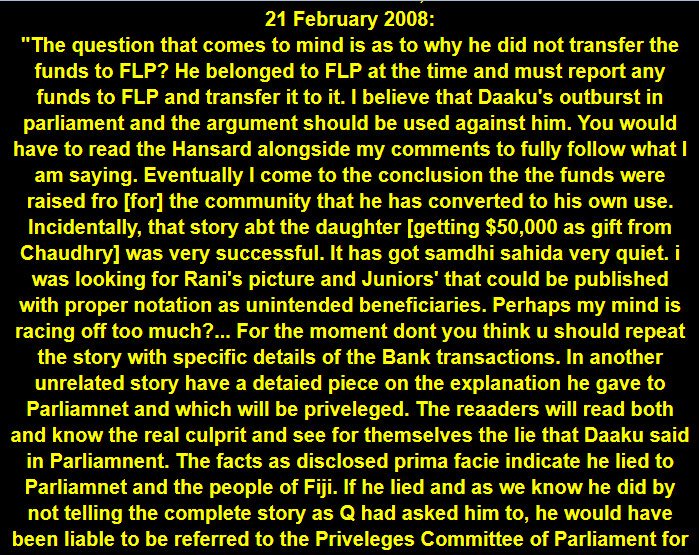

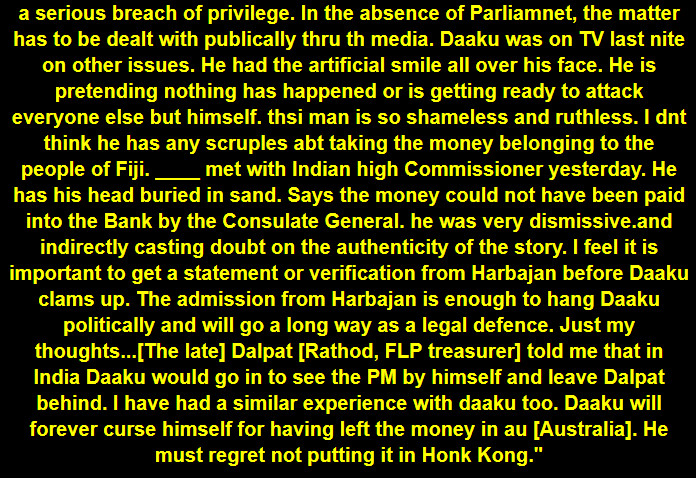

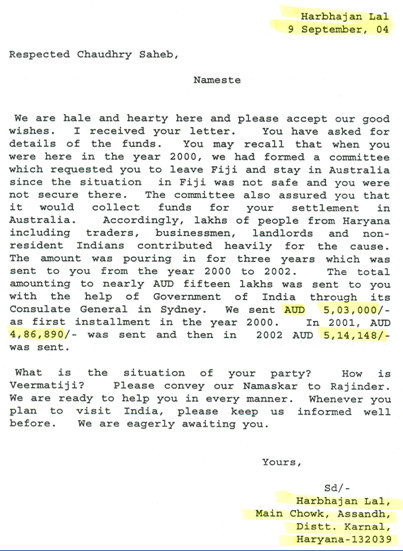

The “Report of Independent Inquiry into the taxation affairs of Mahendra Pal Chaudhry” was prepared by the team that was hastily cobbled together after I disclosed in the Fiji Sun in February 2008 that Chaudhry had been hiding $2million in a secret bank account in Sydney, Australia, and that he had made late lodgement of his 2001, 2002, and 2003 tax returns. Were the late lodgements, I asked, a deliberate ploy on Mr Chaudhry’s part to avoid explaining to FIRCA in 2004 the original source of his $2million in the Australian bank account, which we know originated from India, and was allegedly sent by one Harbhajan Lal of Haryana? I will return to the subject of the New Zealand fund later in the column.

Meanwhile, Chaudhry recently told Fiji TV “Close Up” programme that he did not receive any money from India, even though in March he had claimed on Fiji TV that the money was for him and his family. If we are to accept his denial then the whole inquiry by FIRCA and the three-member team is cancelled out, raising the question of how the inquiry team arrived at its conclusions.

The inquiry team had, based on the 20 September 2004 letter from Harbhajan Lal, concluded in its report that the money came from India: “As noted earlier, in response to FIRCA’s enquiries, Mr Chaudhry and his advisers provided to FIRCA information which ultimately satisfied them that the monies were paid into Mr Chaudhry’s account by the Indian Consulate in Sydney on behalf of supporters of Mr Chaudhry in India, in order to assist him and his family to relocate to Australia consequent on the circumstances surrounding his ceasing to be Prime Minister of Fiji in 2000.”

At the expense of repeating, it is of paramount importance to remind Chaudhry and the nation about the sequence of events which led to the discovery of his secret millions. According to his tax file, in the course of its investigation, FIRCA’s Income Matching Unit (IMU) became aware of his bank accounts in Australia and New Zealand and, on May 11, 2004, wrote to him advising him that they had received information from surveys and banks and financial institutions that he was in receipt of income, which had either not been declared or under declared. He was given 14 days to make representations to FIRCA on receipt of the letter.

On May 18, 2004, Chaudhry wrote to IMU informing it that interest on bank accounts earned in Fiji had been declared in his tax returns and he did not hold any trust deeds. What about the monies abroad? He replied: “In so far as interest from monies held in accounts abroad are concerned, please be advised that these have not been brought to Fiji but remain re-invested in the accounts there.”

On June 3, 2004, the IMU pointed out to him that he had amassed interest and dividends for the year ending 2002 of $29,606.84 and there was a discrepancy of the same amount. On the margins of Chaudhry’s May 18, 2004 letter, certain questions were raised, and the same were later repeated in a letter to him on June 15, 2004. The letter re-iterated that he was required to clarify queries with copies of documentary evidence: (a) the source of funds invested offshore; (b) when did he first invest these monies; (c) details of interest earned from when he first invested; (d) copies of bank statements and documentary evidences of any tax deducted at source.

The next day, June 16, Chaudhry wrote asking for an extension of time to provide the information because “old records will need to be looked up to obtain the details”, and that the banks had requested more time be given.

He also disclosed that he had some commitments and therefore asked if he could be given until August 15, 2004 to furnish the details. FIRCA granted him the requested extension. On August 14, a Suva chartered accountancy firm wrote to FIRCA, notifying it that Chaudhry had appointed the firm to act as his tax agent. The firm asked for further extension till September 15, 2004, which was granted.

On September 3, 2004, representatives from the accountancy firm [G. Lal & Co] visited FIRCA and wanted to know the information that was needed by the tax organisation. They were referred to the letter of June 16, and informed that FIRCA was after the most important detail, and that was “the source of the income”. The accountancy firm stated that the information would be submitted by September 15, 2004. But on September 13, it again wrote to FIRCA asking for further extension until October 15, prompting FIRCA to warn the firm that no further extension would be granted. However, considering that the firm was still awaiting confirmations from Chaudhry, it agreed to the extension but stressed that, “Please be advised that information gathered and “on hand” by your client should be submitted by that date”.

On 4 October, 2004 the accountancy firm wrote to FIRCA enclosing details of the income earned by Chaudhry for the periods based on the documents provided by the banks together with summary of income and withholding taxes deducted at source including: (a) dividend income from Perpetual Investments, Australia; (b) interest income from ANZ, New Zealand: (c) income received from Commonwealth Balanced Fund: (d) interest income from Commonwealth Bank, Australia; (e) income from Colonial First State Investments Limited.

On behalf of Chaudhry, they stated that, “We advise that above income was not included in the tax returns as these contributions and income there from were sourced and earned overseas and the relevant withholding taxes on the income are deducted at source”.

The capital contributions being the deposits in the bank account in the form of donations, they argued, were received from non-residents and attached were the relevant confirmations – Harbhajan Lal’s letter to Chaudhry about the transfer of funds. On October 5, 2004, FIRCA officials met with one of the accountants and according to FIRCA’s office memo they identified details of bank accounts, confirmation of the letter from Harbhajan Lal that the money was raised in India for Chaudhry, and the A$500,000 that was transacted through the Indian Consulate-General in Sydney. One FIRCA officer observed on the office memo: “Transmitted to Australia – How?” and regarding Harbhajan Lal’s letter: “More substantive evidence to support the lttr.”

On October 22, 2004, FIRCA wrote to the accountancy firm regarding the October 5 meeting and for the submission of information the firm had “on hand” at the meeting. FIRCA informed them that they (FIRCA) had examined the documents and would amend the income tax returns for the respective years. However, they would not allow the tax credits due to lack of documentary evidence. FIRCA also emphasised that despite it amending the returns, the tax organisation would still pursue the “source of the funds” issue. “The document submitted explaining the source of the funds is not sufficient enough for our purposes,” it stressed.

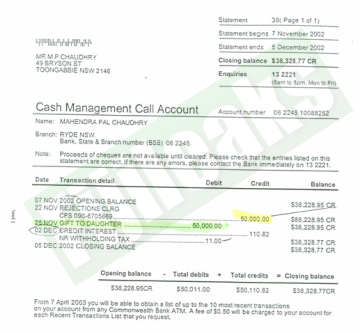

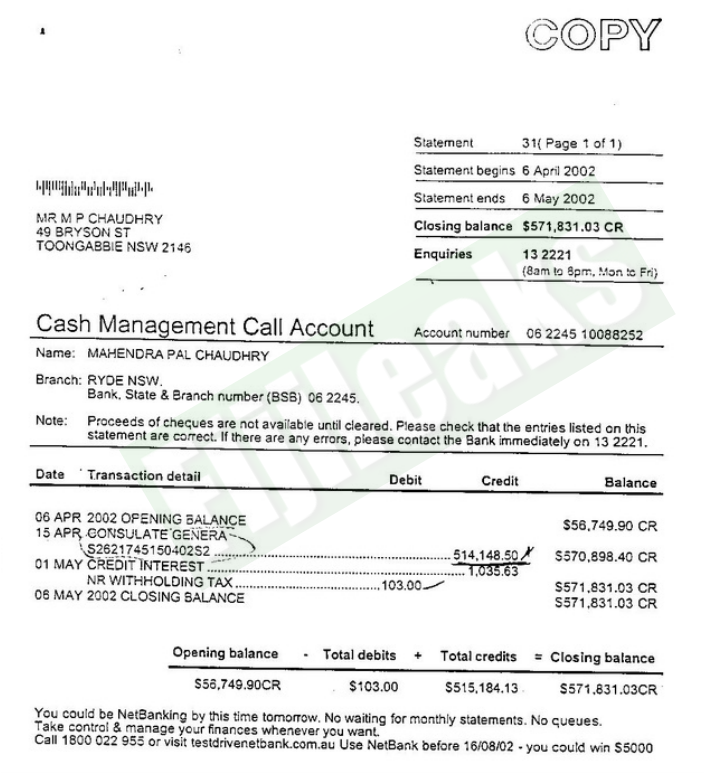

It, therefore, requested the chartered accountancy firm to forward documentary evidences: (a) details of remittances from India to Australia; (b) details of withholding tax deducted; (c) as requested in the letter of 15 June 2004, the copies of bank statements. A copy of the letter was also forwarded to Chaudhry. On November 10, 2004, he paid $86,069.02 in outstanding income tax for 2000. On November 22, 2004, one of the partners in the accountancy firm admitted the payment by the Indian Consulate General of $514,148.50 into Chaudhry’s cash management call account in the Commonwealth Bank of Australia. He also requested FIRCA to make the necessary amendments for the years 2000 to 2003 and the statement of tax account to include credits for the non-resident withholding tax amounting to $22,858.03.

It is instructive to recall that FIRCA and Chaudhry had repeatedly taken shelter behind the confidentiality clause in Section 4 of the Tax Act but as I have argued, the Act does not give the taxpayer the luxury and freedom to hide millions from the nation. I wonder what conclusion we would have drawn from the team’s findings and Chaudhry’s denials if I had not come into possession of his tax file, which also contains details of his New Zealand funds.

Chaudhry's secret New Zealand Bank Account:

On 26 September 2000, Chaudhry had opened an account with ANZ bank in NZ, three months after he was released by George Speight from Parliament. On 1 June 2004, a month after FIRCA began closing in on him, he wrote to the bank requesting interest earned on his account number 981000000116059.

On 16 July, the ANZ bank wrote to him detailing interest he received on the above account between 26 March 2001 and 26 September 2003. Chaudhry received interest income of $NZ23,274.47 or $F24,575.76. The exact amount of funds Chaudhry had in the bank there is not known, but according to forensic accountants, working backwards from the interest he received it was probably $300,000 to $400,000, raising the question of the original source of the New Zealand funds.

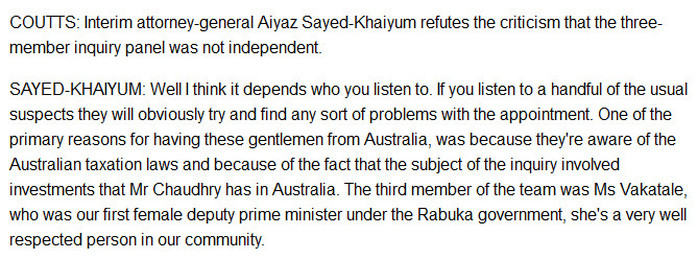

The question that arises is why Aiyaz Sayed-Khaiyum, the Attorney-General, Minister for Justice, Electoral Reform, Public Enterprises and Anti-Corruption, Commerce, Industry and Tourism, has not responded to Chaudhry’s latest denial on Fiji TV, and by extension, to the people of Fiji that no money was received from India? After all, Khaiyum had announced the inquiry team with much fanfare claiming it was being done in the name of good governance, accountability, and transparency.

What has a member of the inquiry team, the local educationist and former Deputy Prime Minister Taufa Vakatale, have to say to Chaudhry’s recent statement on Fiji TV? She might also want to explain why the team concluded that the amount invested by Chaudhry was small? It is time for Fiji’s lawmaker Aiyaz Sayed-Khaiyum to confront Chaudhry’s bluff and bluster while the FLP leader is going around the country preaching about the People’s Charter. Chaudhry should be telling the people of Fiji about his millions, including the source of the funds in his New Zealand bank account. And, who is the “Indian Santa Claus” – one Harbhajan Lal of Haryana, whose letter Chaudhry tendered to FIRCA to convince the tax body that the $2million was from India? In fact, he was only able to invest in the thousands after he received the money in three instalments into his secret Sydney bank account.

There is now a need for a Commission of Enquiry into Chaudhry’s mysterious millions because the three-member team was not constituted under the Commissions of Inquiry Act (Cap47) and, therefore, did not hold any public hearings, call any witnesses nor take any written or oral submissions as to facts or law.

The “Report of Independent Inquiry into the taxation affairs of Mahendra Pal Chaudhry” was prepared by the team that was hastily cobbled together after I disclosed in the Fiji Sun in February 2008 that Chaudhry had been hiding $2million in a secret bank account in Sydney, Australia, and that he had made late lodgement of his 2001, 2002, and 2003 tax returns. Were the late lodgements, I asked, a deliberate ploy on Mr Chaudhry’s part to avoid explaining to FIRCA in 2004 the original source of his $2million in the Australian bank account, which we know originated from India, and was allegedly sent by one Harbhajan Lal of Haryana? I will return to the subject of the New Zealand fund later in the column.

Meanwhile, Chaudhry recently told Fiji TV “Close Up” programme that he did not receive any money from India, even though in March he had claimed on Fiji TV that the money was for him and his family. If we are to accept his denial then the whole inquiry by FIRCA and the three-member team is cancelled out, raising the question of how the inquiry team arrived at its conclusions.

The inquiry team had, based on the 20 September 2004 letter from Harbhajan Lal, concluded in its report that the money came from India: “As noted earlier, in response to FIRCA’s enquiries, Mr Chaudhry and his advisers provided to FIRCA information which ultimately satisfied them that the monies were paid into Mr Chaudhry’s account by the Indian Consulate in Sydney on behalf of supporters of Mr Chaudhry in India, in order to assist him and his family to relocate to Australia consequent on the circumstances surrounding his ceasing to be Prime Minister of Fiji in 2000.”

At the expense of repeating, it is of paramount importance to remind Chaudhry and the nation about the sequence of events which led to the discovery of his secret millions. According to his tax file, in the course of its investigation, FIRCA’s Income Matching Unit (IMU) became aware of his bank accounts in Australia and New Zealand and, on May 11, 2004, wrote to him advising him that they had received information from surveys and banks and financial institutions that he was in receipt of income, which had either not been declared or under declared. He was given 14 days to make representations to FIRCA on receipt of the letter.

On May 18, 2004, Chaudhry wrote to IMU informing it that interest on bank accounts earned in Fiji had been declared in his tax returns and he did not hold any trust deeds. What about the monies abroad? He replied: “In so far as interest from monies held in accounts abroad are concerned, please be advised that these have not been brought to Fiji but remain re-invested in the accounts there.”

On June 3, 2004, the IMU pointed out to him that he had amassed interest and dividends for the year ending 2002 of $29,606.84 and there was a discrepancy of the same amount. On the margins of Chaudhry’s May 18, 2004 letter, certain questions were raised, and the same were later repeated in a letter to him on June 15, 2004. The letter re-iterated that he was required to clarify queries with copies of documentary evidence: (a) the source of funds invested offshore; (b) when did he first invest these monies; (c) details of interest earned from when he first invested; (d) copies of bank statements and documentary evidences of any tax deducted at source.

The next day, June 16, Chaudhry wrote asking for an extension of time to provide the information because “old records will need to be looked up to obtain the details”, and that the banks had requested more time be given.

He also disclosed that he had some commitments and therefore asked if he could be given until August 15, 2004 to furnish the details. FIRCA granted him the requested extension. On August 14, a Suva chartered accountancy firm wrote to FIRCA, notifying it that Chaudhry had appointed the firm to act as his tax agent. The firm asked for further extension till September 15, 2004, which was granted.

On September 3, 2004, representatives from the accountancy firm [G. Lal & Co] visited FIRCA and wanted to know the information that was needed by the tax organisation. They were referred to the letter of June 16, and informed that FIRCA was after the most important detail, and that was “the source of the income”. The accountancy firm stated that the information would be submitted by September 15, 2004. But on September 13, it again wrote to FIRCA asking for further extension until October 15, prompting FIRCA to warn the firm that no further extension would be granted. However, considering that the firm was still awaiting confirmations from Chaudhry, it agreed to the extension but stressed that, “Please be advised that information gathered and “on hand” by your client should be submitted by that date”.

On 4 October, 2004 the accountancy firm wrote to FIRCA enclosing details of the income earned by Chaudhry for the periods based on the documents provided by the banks together with summary of income and withholding taxes deducted at source including: (a) dividend income from Perpetual Investments, Australia; (b) interest income from ANZ, New Zealand: (c) income received from Commonwealth Balanced Fund: (d) interest income from Commonwealth Bank, Australia; (e) income from Colonial First State Investments Limited.

On behalf of Chaudhry, they stated that, “We advise that above income was not included in the tax returns as these contributions and income there from were sourced and earned overseas and the relevant withholding taxes on the income are deducted at source”.

The capital contributions being the deposits in the bank account in the form of donations, they argued, were received from non-residents and attached were the relevant confirmations – Harbhajan Lal’s letter to Chaudhry about the transfer of funds. On October 5, 2004, FIRCA officials met with one of the accountants and according to FIRCA’s office memo they identified details of bank accounts, confirmation of the letter from Harbhajan Lal that the money was raised in India for Chaudhry, and the A$500,000 that was transacted through the Indian Consulate-General in Sydney. One FIRCA officer observed on the office memo: “Transmitted to Australia – How?” and regarding Harbhajan Lal’s letter: “More substantive evidence to support the lttr.”

On October 22, 2004, FIRCA wrote to the accountancy firm regarding the October 5 meeting and for the submission of information the firm had “on hand” at the meeting. FIRCA informed them that they (FIRCA) had examined the documents and would amend the income tax returns for the respective years. However, they would not allow the tax credits due to lack of documentary evidence. FIRCA also emphasised that despite it amending the returns, the tax organisation would still pursue the “source of the funds” issue. “The document submitted explaining the source of the funds is not sufficient enough for our purposes,” it stressed.

It, therefore, requested the chartered accountancy firm to forward documentary evidences: (a) details of remittances from India to Australia; (b) details of withholding tax deducted; (c) as requested in the letter of 15 June 2004, the copies of bank statements. A copy of the letter was also forwarded to Chaudhry. On November 10, 2004, he paid $86,069.02 in outstanding income tax for 2000. On November 22, 2004, one of the partners in the accountancy firm admitted the payment by the Indian Consulate General of $514,148.50 into Chaudhry’s cash management call account in the Commonwealth Bank of Australia. He also requested FIRCA to make the necessary amendments for the years 2000 to 2003 and the statement of tax account to include credits for the non-resident withholding tax amounting to $22,858.03.

It is instructive to recall that FIRCA and Chaudhry had repeatedly taken shelter behind the confidentiality clause in Section 4 of the Tax Act but as I have argued, the Act does not give the taxpayer the luxury and freedom to hide millions from the nation. I wonder what conclusion we would have drawn from the team’s findings and Chaudhry’s denials if I had not come into possession of his tax file, which also contains details of his New Zealand funds.

Chaudhry's secret New Zealand Bank Account:

On 26 September 2000, Chaudhry had opened an account with ANZ bank in NZ, three months after he was released by George Speight from Parliament. On 1 June 2004, a month after FIRCA began closing in on him, he wrote to the bank requesting interest earned on his account number 981000000116059.

On 16 July, the ANZ bank wrote to him detailing interest he received on the above account between 26 March 2001 and 26 September 2003. Chaudhry received interest income of $NZ23,274.47 or $F24,575.76. The exact amount of funds Chaudhry had in the bank there is not known, but according to forensic accountants, working backwards from the interest he received it was probably $300,000 to $400,000, raising the question of the original source of the New Zealand funds.

The question that arises is why Aiyaz Sayed-Khaiyum, the Attorney-General, Minister for Justice, Electoral Reform, Public Enterprises and Anti-Corruption, Commerce, Industry and Tourism, has not responded to Chaudhry’s latest denial on Fiji TV, and by extension, to the people of Fiji that no money was received from India? After all, Khaiyum had announced the inquiry team with much fanfare claiming it was being done in the name of good governance, accountability, and transparency.

What has a member of the inquiry team, the local educationist and former Deputy Prime Minister Taufa Vakatale, have to say to Chaudhry’s recent statement on Fiji TV? She might also want to explain why the team concluded that the amount invested by Chaudhry was small? It is time for Fiji’s lawmaker Aiyaz Sayed-Khaiyum to confront Chaudhry’s bluff and bluster while the FLP leader is going around the country preaching about the People’s Charter. Chaudhry should be telling the people of Fiji about his millions, including the source of the funds in his New Zealand bank account. And, who is the “Indian Santa Claus” – one Harbhajan Lal of Haryana, whose letter Chaudhry tendered to FIRCA to convince the tax body that the $2million was from India? In fact, he was only able to invest in the thousands after he received the money in three instalments into his secret Sydney bank account.

There is now a need for a Commission of Enquiry into Chaudhry’s mysterious millions because the three-member team was not constituted under the Commissions of Inquiry Act (Cap47) and, therefore, did not hold any public hearings, call any witnesses nor take any written or oral submissions as to facts or law.

The above is extracted from the 60 page submission to DDP's Office: Perjury probe request in Mahendra Chaudhry’s affidavit before Justice Daniel Goundar in the Fiji High Court and call for other criminal investigations arising out of Mr Chaudhry’s income tax file By VICTOR LAL and RUSSELL HUNTER, 12 September 2012

The case against the Petitioner [Mahendra Pal Chaudhry] went to trial on the following charges contained in the amended information dated 3rd October 2013, extracted from Fiji Supreme Court:

FIRST COUNT

Statement of Offence

FAILURE TO SURRENDER FOREIGN CURRENCY: Contrary to Section 4 of the Exchange Control Act, Cap 211 and section 1 of Part II of the Fifth Schedule of the Exchange Control Act, Cap 211.

Particulars of Offence

MAHENDRA PAL CHAUDHRY in between the 1st day of November 2000 and the 23rd day of July 2010, at Suva in the Central Division being a resident in Fiji entitled to sell foreign currency but not being an authorised dealer, however being required by law to offer it for sale to an authorized dealer, retained the sum of $1,500,000.00 ($1.5 million) Australian Dollars for his own use and benefit, without the consent of the Governor of the Reserve Bank of Fiji.

SECOND COUNT

Statement of Offence

DEALING IN FOREIGN CURRENCY OTHERWISE THAN WITH AN AUTHORISED DEALER WITHOUT PERMISSION: Contrary to Section 3 of the Exchange Control Act, Cap 211 and section 1 of Part II of the Fifth Schedule of the Exchange Control Act, Cap 211.

Particulars of Offence

MAHENDRA PAL CHAUDHRY in between the 1st day of November 2000 and the 23rd day of July 2010, at Suva in the Central Division being a resident in Fiji but not being an authorised dealer, did lend the sum of $1,500,000.00 ($1.5 million) Australian Dollars to persons otherwise than an authorized dealer, namely the Financial Institutions in Australia and New Zealand as listed in Annexure marked "A", without the permission of the Governor of the Reserve Bank of Fiji.

THIRD COUNT

Statement of Offence

FAILURE TO COLLECT DEBTS: Contrary to Section 26(1)(a) of the Exchange Control Act, Cap 211 and section 1 of Part II of the Fifth Schedule of the Exchange Control Act,http://www.paclii.org/fj/legis/consol_act/eca170/ Cap 211.

Particulars of Offence

MAHENDRA PAL CHAUDHRY in between the 1st day of November 2000 and the 23rd day of July 2010, at Suva in the Central Division being a resident in Fiji having the right to receive a sum of $1,500,000.00 ($1.5 million) Australian Dollars from the Financial Institutions in Australia and New Zealand as listed in Annexure marked "A", caused the delay of payment of the said sum, in whole or in part, to himself by authorizing the continual re-investment of the said sum together with interest acquired back into the said Financial Institutions without the consent of the Governor of the Reserve Bank of Fiji."

http://www.paclii.org/cgi-bin/sinodisp/fj/cases/FJSC/2014/14.html?stem=&synonyms=&query=mahendra%20pal%20chaudhry

FIRST COUNT

Statement of Offence

FAILURE TO SURRENDER FOREIGN CURRENCY: Contrary to Section 4 of the Exchange Control Act, Cap 211 and section 1 of Part II of the Fifth Schedule of the Exchange Control Act, Cap 211.

Particulars of Offence

MAHENDRA PAL CHAUDHRY in between the 1st day of November 2000 and the 23rd day of July 2010, at Suva in the Central Division being a resident in Fiji entitled to sell foreign currency but not being an authorised dealer, however being required by law to offer it for sale to an authorized dealer, retained the sum of $1,500,000.00 ($1.5 million) Australian Dollars for his own use and benefit, without the consent of the Governor of the Reserve Bank of Fiji.

SECOND COUNT

Statement of Offence

DEALING IN FOREIGN CURRENCY OTHERWISE THAN WITH AN AUTHORISED DEALER WITHOUT PERMISSION: Contrary to Section 3 of the Exchange Control Act, Cap 211 and section 1 of Part II of the Fifth Schedule of the Exchange Control Act, Cap 211.

Particulars of Offence

MAHENDRA PAL CHAUDHRY in between the 1st day of November 2000 and the 23rd day of July 2010, at Suva in the Central Division being a resident in Fiji but not being an authorised dealer, did lend the sum of $1,500,000.00 ($1.5 million) Australian Dollars to persons otherwise than an authorized dealer, namely the Financial Institutions in Australia and New Zealand as listed in Annexure marked "A", without the permission of the Governor of the Reserve Bank of Fiji.

THIRD COUNT

Statement of Offence

FAILURE TO COLLECT DEBTS: Contrary to Section 26(1)(a) of the Exchange Control Act, Cap 211 and section 1 of Part II of the Fifth Schedule of the Exchange Control Act,http://www.paclii.org/fj/legis/consol_act/eca170/ Cap 211.

Particulars of Offence

MAHENDRA PAL CHAUDHRY in between the 1st day of November 2000 and the 23rd day of July 2010, at Suva in the Central Division being a resident in Fiji having the right to receive a sum of $1,500,000.00 ($1.5 million) Australian Dollars from the Financial Institutions in Australia and New Zealand as listed in Annexure marked "A", caused the delay of payment of the said sum, in whole or in part, to himself by authorizing the continual re-investment of the said sum together with interest acquired back into the said Financial Institutions without the consent of the Governor of the Reserve Bank of Fiji."

http://www.paclii.org/cgi-bin/sinodisp/fj/cases/FJSC/2014/14.html?stem=&synonyms=&query=mahendra%20pal%20chaudhry

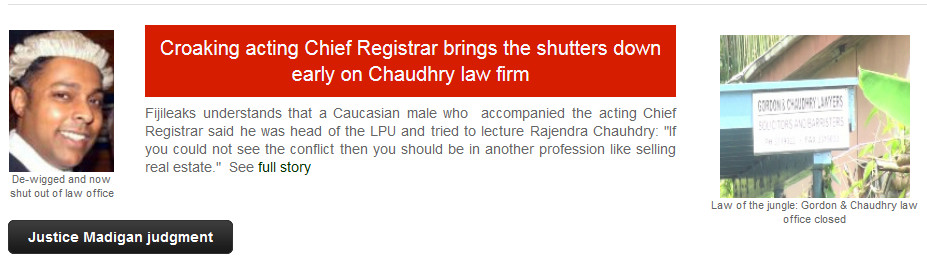

Rajendra Chaudhry had filed and had succeeded on all grounds of his appeal against his office closure in Fiji. He has since sued the Chief Registrar, Mohammed Saneem and Ba lawyer Shalen Krishna for their part in his office closure.

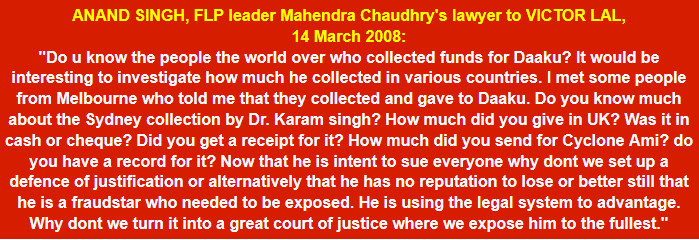

Fijileaks: Eight years later Mahendra Chaudhry remains tight-lipped about the origins of the funds in his secret bank account in New Zealand! Anand Singh, one of the most eager of lawyers who kept badgering Victor Lal to reach deep into Mahendra Chauhdry's secret millions (see Singh to Lal below) surfaced to defend Chaudhry without any hesitation, raising questions whether he was "a planted mole" - lately he also turned up at Rajendra Chaudhry's new law firm in Auckland, New Zealand

|  |

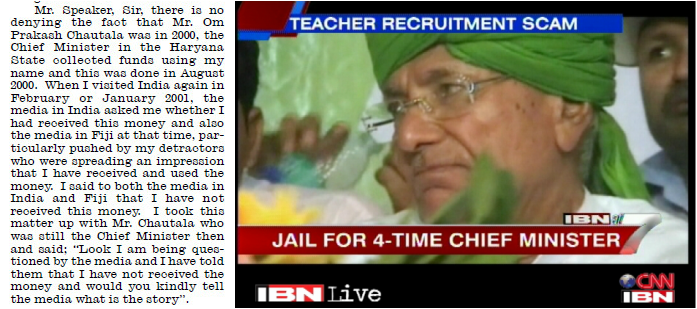

Om Prakash Chautala jailed

|   |

|  |

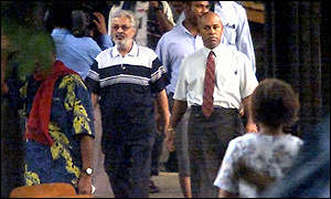

BATTING FOR NOT GUILTY VERDICT: Anand Singh on way to Fiji High Court with Chaudhry during the tax evasion trial